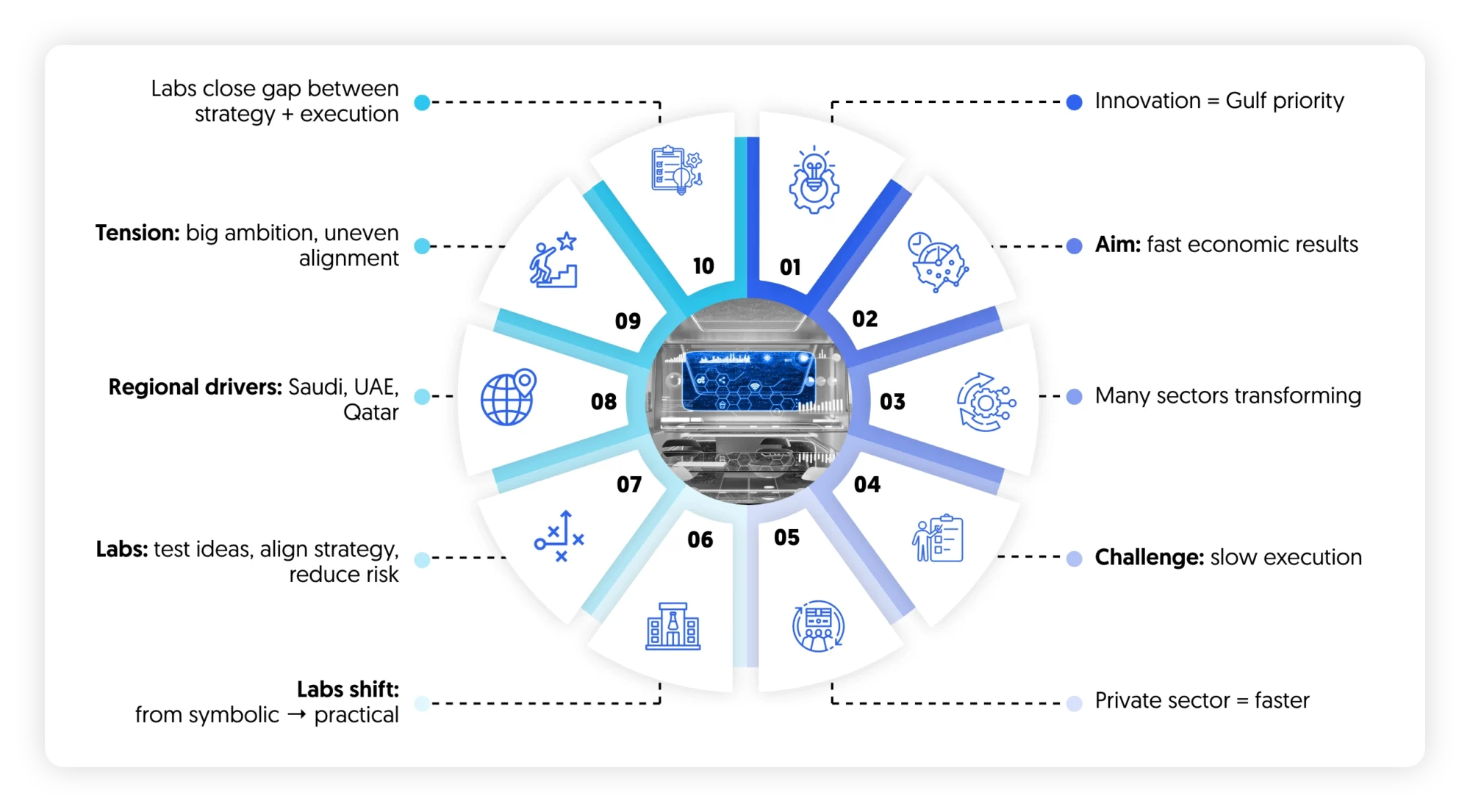

Across the Gulf, “innovation” has shifted from a talking point to a line item on national balance sheets. Governments are no longer asking whether they should invest in innovation, but how quickly those investments can translate into economic value. The scale is unprecedented. Entire sectors are being redesigned in parallel energy, mobility, finance, public services, alongside rapidly expanding domains such as tourism, destination development, future cities, and sports often under tight timelines and public scrutiny.

Yet beneath the ambition, a quieter challenge is emerging. Strategies are clear, funding is available, and mandates are strong, but execution does not always keep pace. Large transformation programs tend to move through layers of policy, procurement, and legacy systems before they reach something tangible. At the same time, private sector players startups, scale-ups, and even large corporates operate on very different cycles. They optimize for speed, iteration, and market signals, not policy alignment.

This is where innovation labs are beginning to take on a more critical role than originally intended.

In their earliest form, many labs in the region were positioned as symbolic spaces to signal modernity, creativity, or alignment with global trends. That phase is ending. The current environment is less forgiving. Budgets are scrutinized, outcomes are expected, and initiatives that do not translate into measurable impact are quickly deprioritized.

What is emerging instead is a different kind of innovation lab. One that sits closer to execution than ideation. One that is designed not to generate ideas in isolation, but to test, validate, and adapt them within the constraints of real systems regulatory, operational, and commercial.

In this sense, innovation labs are becoming less about creativity and more about orchestration. They act as platforms that align strategy with execution, prioritizing initiatives based on value potential, stress-testing ideas against real-world constraints, and shaping clearer pathways from concept to implementation.

They create a controlled environment where government entities can engage with private sector capabilities without committing to full-scale deployment. They allow corporates to navigate regulatory ambiguity without taking on disproportionate risk. They offer a space where assumptions on user behavior, technology performance, or policy impact can be challenged early, before significant capital is deployed.

The timing of this shift is not incidental. As Saudi Vision 2030 accelerates large-scale transformation, the United Arab Emirates continues to refine its position as a global innovation hub, and Qatar advances its own diversification agenda through national development programs, the region is encountering a shared structural tension. Ambition is high, but alignment across stakeholders remains uneven. The gap is more operational than conceptual.

Innovation labs, when designed with intent, begin to close that gap.

They do not replace strategy, nor do they substitute for execution. What they do is reduce the distance between the two.

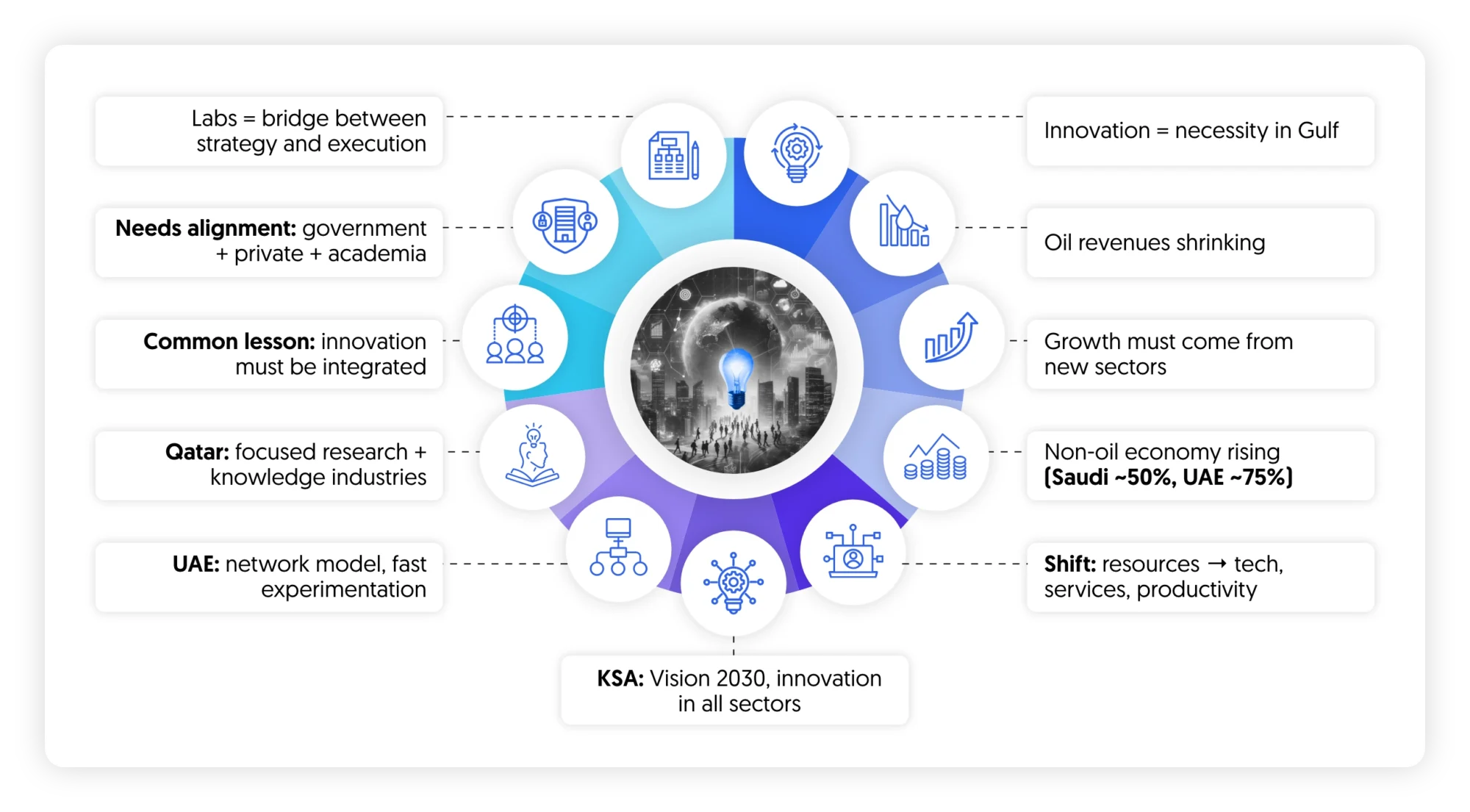

The Macro Shift: Innovation as National Strategy

The push toward innovation in the Gulf is often framed as ambition. In reality, it is closer to necessity.

Hydrocarbon revenues once provided both stability and flexibility. Governments could fund large-scale development while absorbing inefficiencies in execution. That buffer is narrowing. Population growth, global competition, and the long-term uncertainty around energy markets are forcing a more disciplined approach to economic design. Growth now needs to come from sectors that behave very differently from oil more dynamic, more competitive, and far less predictable.

This shift is already visible in the data. Across the GCC, non-oil sectors are contributing an increasing share of GDP, with Saudi Arabia’s non-oil economy now accounting for roughly half of total output and continuing to grow at a faster pace than the oil sector. In the United Arab Emirates, non-oil activities contribute close to three-quarters of GDP, driven by services, trade, tourism, and financial sectors. What sits beneath these numbers is not just diversification, but a gradual reconfiguration of how value is created away from resource extraction and toward productivity, technology, and services.

This is the context in which national innovation strategies have taken shape.

In Saudi Vision 2030, innovation is not positioned as a standalone pillar. It is embedded across sectors: logistics, healthcare, tourism, manufacturing, and financial services. The objective is not simply to create new industries, but to reconfigure how existing ones operate. Digital infrastructure, artificial intelligence, and advanced manufacturing are being deployed as levers to increase productivity and attract external investment.

Execution is supported by a network of national entities. The Public Investment Fund acts as both financier and market maker, shaping demand in strategic sectors. At the same time, institutions such as the Digital Government Authority and the Research, Development and Innovation Authority are building the regulatory and research backbone required to sustain innovation over time. Together, these entities are not only funding transformation, but structuring how it unfolds.

This creates momentum, but it also introduces concentration. Decision-making tends to be centralized, which can accelerate direction-setting while adding complexity when initiatives move into execution across multiple stakeholders.

In the UAE, the trajectory has been different. Rather than building scale first, the focus has been on creating an environment where innovation can circulate more freely. Entities such as the Dubai Future Foundation and regulatory platforms like the Abu Dhabi Global Market have prioritized experimentation. Financial ecosystems such as the Dubai International Financial Centre further reinforce this model, acting as platforms where startups, investors, and corporates can interact within a structured yet flexible environment.

The result is a system that behaves more like a network than a hierarchy. Innovation is not confined to national programs; it emerges through interactions between startups, regulators, investors, and global partners. This has allowed the UAE to move quickly in areas such as fintech, digital assets, and AI governance, often setting precedents that others in the region observe before adopting.

In Qatar, the model is more targeted. National efforts focus on building depth in selected sectors, with a strong emphasis on research, education, and knowledge-based industries. Institutions and platforms are being used to translate research into applied innovation, particularly in areas such as technology, sports, and advanced industries. Rather than pursuing broad-based transformation at scale, the approach prioritizes concentrated bets where global relevance can be achieved.

Despite these differences, these models are converging on a similar realization.

Innovation cannot be treated as an external layer applied to the economy. It has to be integrated into how institutions operate, how regulations are designed, and how capital is deployed. This requires orchestration across actors that historically have not worked closely together government entities, private enterprises, academia, and entrepreneurs.

That orchestration does not happen automatically.

It requires mechanisms, structures, and environments where alignment can be built in practice, not just defined in policy. This is where innovation labs begin to intersect with national strategy not as an accessory, but as part of the operating model.

How Much Is Being Spent on Innovation?

The scale of investment in innovation across the Gulf is often cited, but less frequently unpacked. Headline numbers trillions in regional transformation commitments can obscure a more important question: how much of that capital is actually directed toward building innovation capacity, and how effectively it is being deployed.

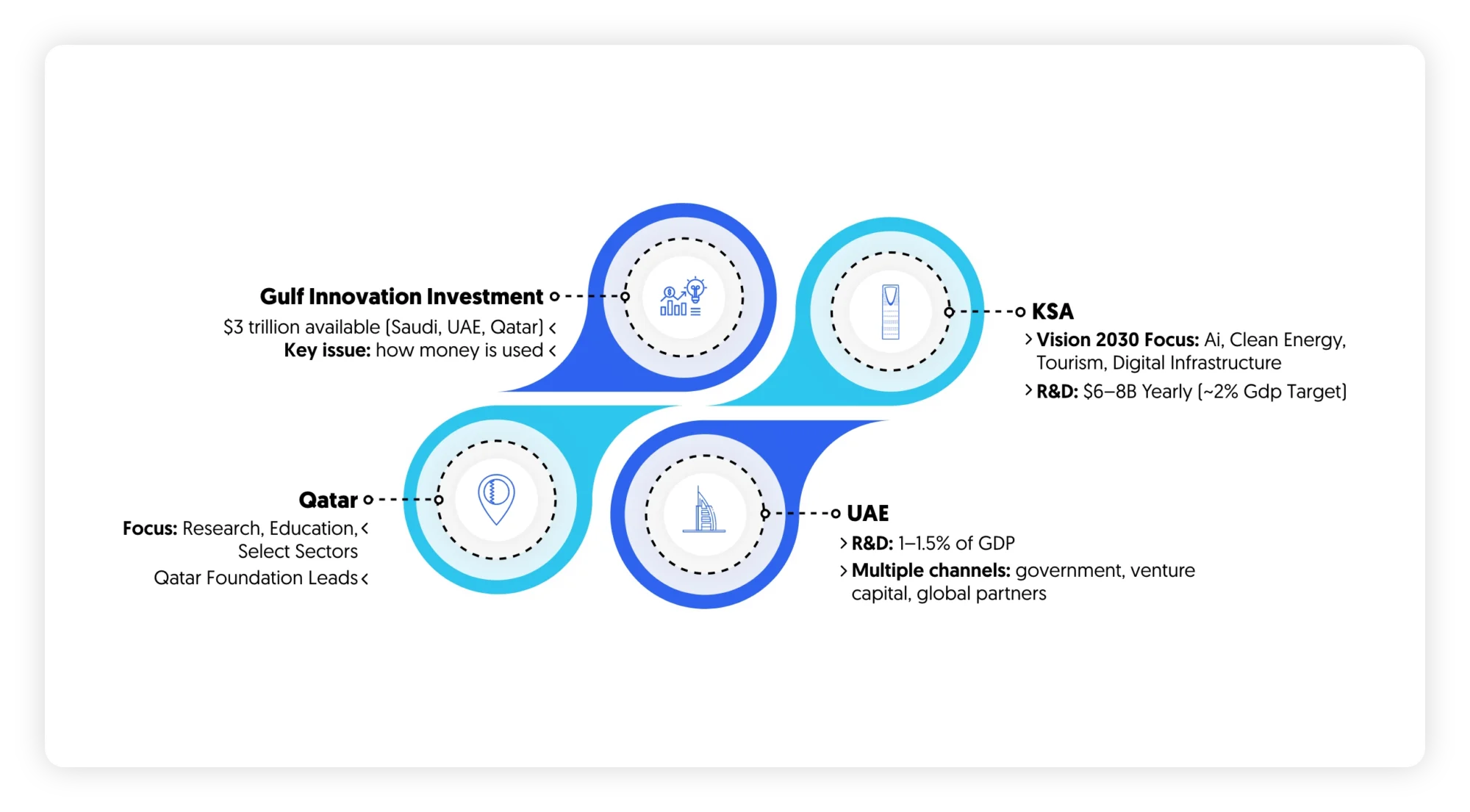

Across the GCC, combined sovereign wealth and transformation-related investment capacity exceeds $3 trillion, concentrated primarily in Saudi Arabia, the UAE, and to a smaller but increasingly strategic extent, Qatar. Within this, innovation-related spending is not always isolated as a standalone budget line, but embedded across national transformation programs, sector strategies, and sovereign investment vehicles.

In Saudi Arabia, spending on innovation sits within a broader economic reconfiguration rather than a single, clearly defined allocation. Under Saudi Vision 2030, capital is flowing into sectors expected to generate long-term productivity gains advanced manufacturing, artificial intelligence, clean energy, tourism, and digital infrastructure. Estimates place annual R&D expenditure in the range of $6–8 billion, with an ambition to increase R&D intensity toward ~2% of GDPover the medium term.

That target is significant in a regional context where research intensity has historically remained below global innovation economies.

What is notable is not just the amount, but the structure. A large share of this investment is being channeled through the Public Investment Fund, which blends commercial objectives with national priorities. This enables rapid deployment of capital into strategic sectors, but also means innovation funding is often tied to large-scale, programmatic investments. As a result, experimentation tends to occur within defined strategic corridors rather than through highly distributed, bottom-up mechanisms.

In the UAE, the absolute scale of R&D investment is smaller, but more diversified relative to GDP structure. R&D spending is estimated at around 1–1.5% of GDP, with continued upward momentum driven by both public and private sector participation. More importantly, capital flows through multiple channels rather than a single dominant vehicle. Government programs coexist with venture capital, corporate R&D, and international partnerships.

Dubai Future Foundation plays a role in funding and enabling pilot initiatives, while financial ecosystems like the Abu Dhabi Global Market and the Dubai International Financial Centre attract global capital into emerging sectors. This creates a system where innovation funding is not only deployed, but circulated allowing ideas to move across multiple entry points before scaling.

In Qatar, investment is more concentrated and selective. Rather than scaling broad-based innovation spending, capital is directed toward specific national priorities, particularly research, education, and targeted high-impact sectors. Institutions such as Qatar Foundation and related research ecosystems channel funding into areas like technology, sports science, and knowledge-based industries. The model is less about volume and more about precision focusing resources where global differentiation can realistically be achieved.

Across these three models, a pattern begins to emerge.

There is no shortage of funding. Capital availability is one of the region’s structural advantages. The constraint lies in how that capital is structured and translated into capability. Innovation spending is often distributed across ministries, sovereign funds, and national programs that operate with different mandates and timelines. Without strong alignment mechanisms, this can lead to duplication in some areas and underinvestment in others.

A second layer of complexity comes from how success is defined. Large investments tend to prioritize visibility flagship projects, infrastructure, and national announcements. These are important for signaling intent, but they do not always translate into sustained innovation capacity. Smaller, iterative efforts testing business models, refining regulatory frameworks, and adapting technologies to local context often receive comparatively less focus, despite being critical for long-term ecosystem maturity.

This gap is becoming more visible as programs mature.

The conversation is gradually shifting from how much is being invested to how effectively those investments are converted into outcomes not just financial returns, but capabilities: skilled talent, adaptable institutions, and ecosystems that can sustain innovation beyond initial funding cycles.

Bridging that gap between capital and capability is where more targeted, execution-focused mechanisms begin to matter.

Government Innovation Ecosystems

At a structural level, Saudi Arabia and the UAE are solving for the same outcome diversified, innovation-driven economies. The way they are organizing their ecosystems to get there reflects two distinct operating philosophies.

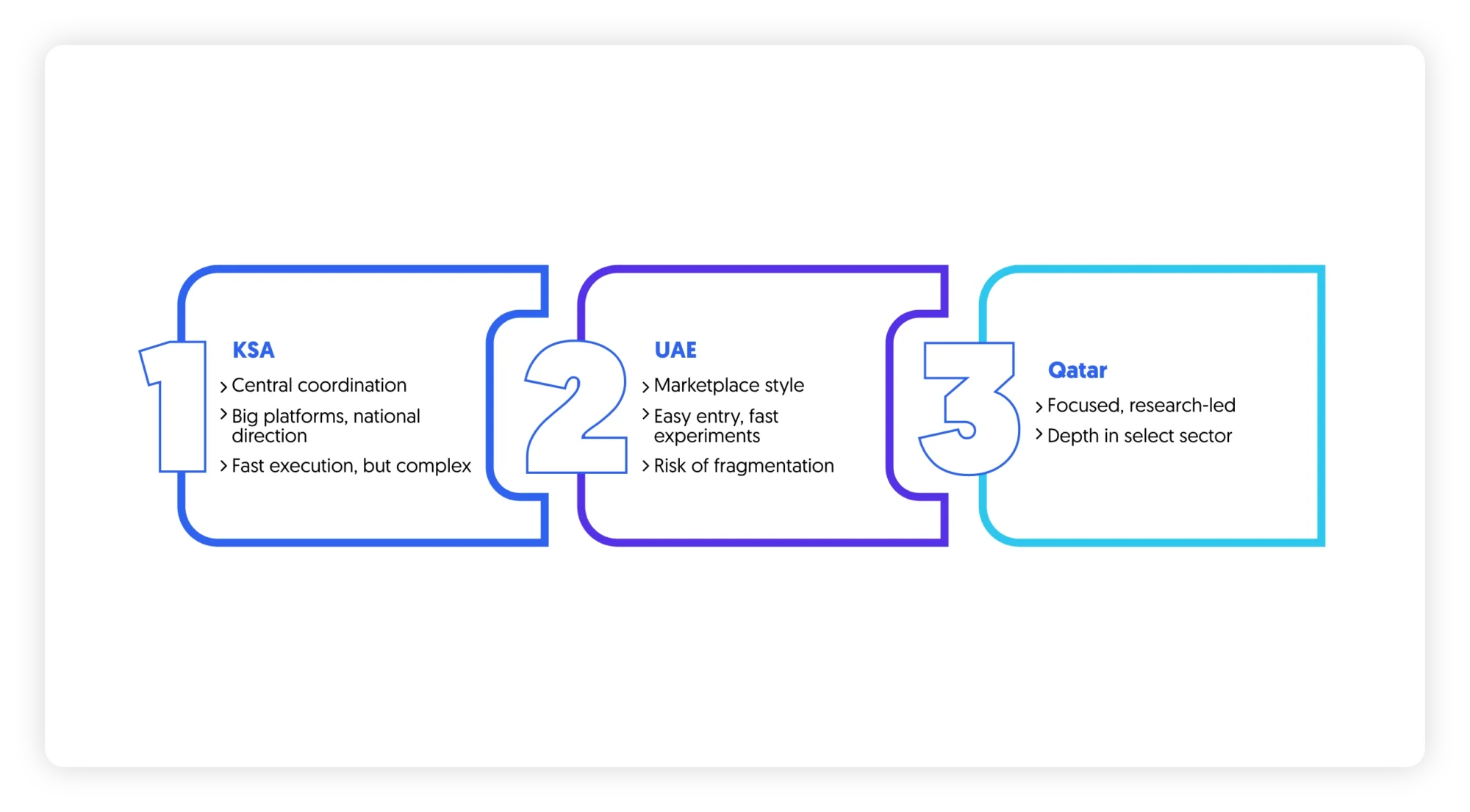

In Saudi Arabia, the model is anchored in scale and central coordination.

Saudi Data and AI Authority and the Digital Government Authority set national direction, build core digital infrastructure, and standardize how transformation unfolds across sectors. A critical but often underemphasized layer is the Research, Development and Innovation Authority, which plays a central role in shaping the national R&D agenda, enabling technology transfer, and aligning research output with industrial priorities.

This ecosystem is complemented by the financial weight of the Public Investment Fund, which operates as both investor and ecosystem architect, actively shaping demand across strategic sectors.

The advantage of this model is momentum. When priorities are defined centrally, execution can move quickly at scale. Entire sectors can be reoriented in a relatively short period, supported by aligned funding, regulation, and institutional backing.

The trade-off is complexity at the edges. As initiatives move from national platforms into sector-specific or operational contexts, coordination becomes more challenging. Different entities may be working toward similar objectives, but with varying timelines, incentives, and interpretations of success. For private sector participants, navigating this landscape often requires significant effort not because opportunities are limited, but because pathways into the system are not always clearly structured.

In contrast, the UAE has built an ecosystem that behaves more like a marketplace.

Organizations such as the Dubai Future Foundation focus on creating entry points rather than directing outcomes. Regulatory environments like the Abu Dhabi Global Market are designed to attract global players by offering clarity, flexibility, and speed. Financial and innovation hubs such as the Dubai International Financial Centre further reinforce this model by enabling startups, corporates, and investors to operate within a tightly integrated yet open ecosystem.

The emphasis is less on controlling the direction of innovation and more on enabling it to emerge through interaction.

This model lowers the barrier to participation. Startups, corporates, and international firms can test ideas, enter the market, and scale solutions with relatively fewer structural constraints. It also allows the UAE to respond quickly to global trends, often positioning itself as an early adopter in areas such as fintech, digital assets, and advanced technologies.

The trade-off here is different. A more distributed system can lead to fragmentation if not carefully managed. Without strong alignment mechanisms, innovation efforts may remain concentrated within specific hubs or sectors, limiting their broader systemic impact.

What becomes clear when comparing these ecosystems is that neither model is inherently superior. Each is optimized for a different dimension of ecosystem development.

Saudi Arabia is building depth large platforms, national capabilities, and sector-wide transformation. The UAE is optimizing flow ease of entry, speed of experimentation, and global connectivity.

Both, however, begin to converge on a similar structural challenge.

As ecosystems grow more complex, the distance between stakeholders increases. Government entities, regulators, corporates, startups, and investors operate within the same system, but not always in sync. Priorities diverge, timelines shift, and opportunities can stall in the space between intention and execution.

In this broader regional context, Qatar represents a third, more targeted model. Rather than scaling across breadth or optimizing for flow, its approach concentrates on depth building capability in selected sectors through research-led institutions and focused national initiatives. This creates a different type of ecosystem dynamic, one where innovation is tightly linked to long-term knowledge creation and sector specialization.

Closing the distance between these different actors and models requires more than policy alignment or capital allocation. It requires environments where stakeholders can engage directly, test assumptions, and move from concept to implementation without the usual institutional lag.

This is where the conversation shifts from ecosystem design to how these ecosystems actually function in practice.

The Role of Innovation Labs in Bridging Public & Private Sectors

If the previous sections describe the architecture of innovation in the region, this is where the stress points become visible.

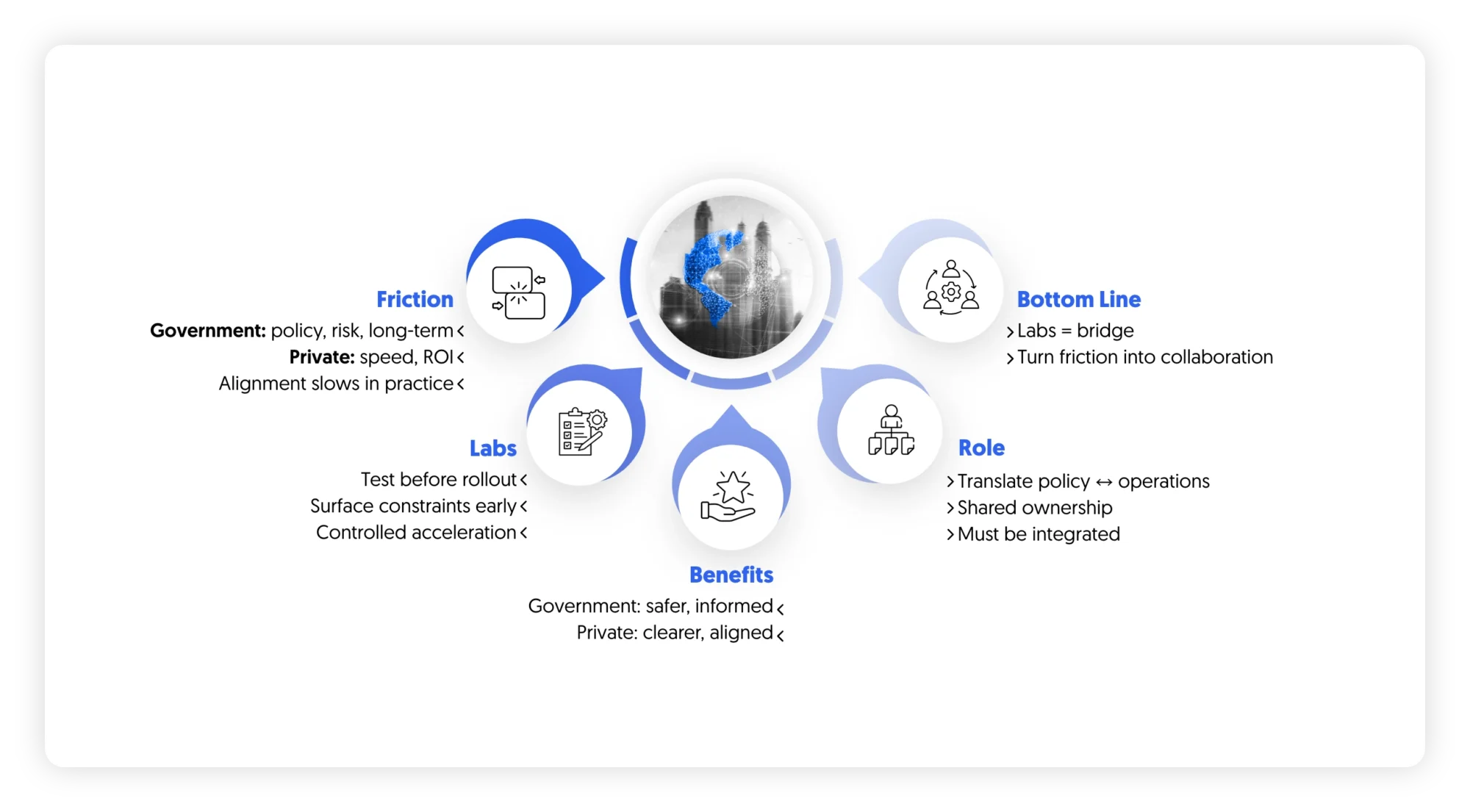

Public and private actors are increasingly operating within the same strategic space, but they are not calibrated the same way. Government entities are accountable to policy, risk management, and long-term national outcomes. Private sector players are driven by timelines, competitive pressure, and return on investment. Both are necessary. The friction lies in how they interact.

This friction tends to surface at predictable moments.

A government entity defines a priority digital identity, smart mobility, AI-enabled services and allocates funding. A private company has a solution, or at least a strong hypothesis. On paper, the alignment is clear. In practice, progress slows down. Procurement cycles extend, requirements evolve, regulatory interpretations shift, and what began as a focused initiative becomes diluted over time.

Innovation labs, when they function properly, intervene at this exact point.

They create a space where engagement happens before full commitment. Instead of moving directly from concept to large-scale deployment, ideas are tested in contained environments. Assumptions are made explicit. Constraints technical, regulatory, operational are surfaced early rather than discovered mid-implementation.

The value here is not speed for its own sake. It is controlled acceleration.

For government entities, this means the ability to explore new approaches without exposing core systems or public services to unnecessary risk. Policies can be stress-tested against real use cases. Technologies can be evaluated in context, not just in theory. Decisions become more informed, and therefore more defensible.

For private sector participants, the benefit is access with clarity. Rather than navigating opaque processes or waiting for formal tenders, they engage directly with the problem space. They understand not just what is being asked, but why. This reduces misalignment and increases the likelihood that what is built will actually be adopted.

The most effective labs go a step further. They do not just test ideas; they translate between worlds.

They take policy language and convert it into operational requirements. They take technical capabilities and frame them in terms that align with regulatory and institutional realities. This translation layer is often overlooked, yet it is where many initiatives either gain traction or stall.

There is also a subtler function at play.

Innovation labs create shared ownership. When multiple stakeholders are involved in shaping and testing a solution from the outset, the outcome is less likely to be perceived as externally imposed. This matters in environments where adoption depends on coordination across entities, not just top-down directives.

None of this happens automatically. Labs that operate as isolated units detached from decision-makers or disconnected from real implementation pathways tend to produce outputs that do not travel far. The difference lies in how closely they are integrated into the broader system.

When positioned correctly, innovation labs are not parallel structures. They are connective tissue.

They do not eliminate the structural differences between public and private sectors, but they make those differences manageable. More importantly, they turn potential friction into something productive a space where ideas are refined, aligned, and made executable before significant capital and time are committed.

Research, Regulation & Ecosystem Development

As innovation agendas mature across the region, attention is shifting toward a less visible layer of the system: the interplay between research, regulation, and market development. This is where long-term competitiveness is either built or constrained.

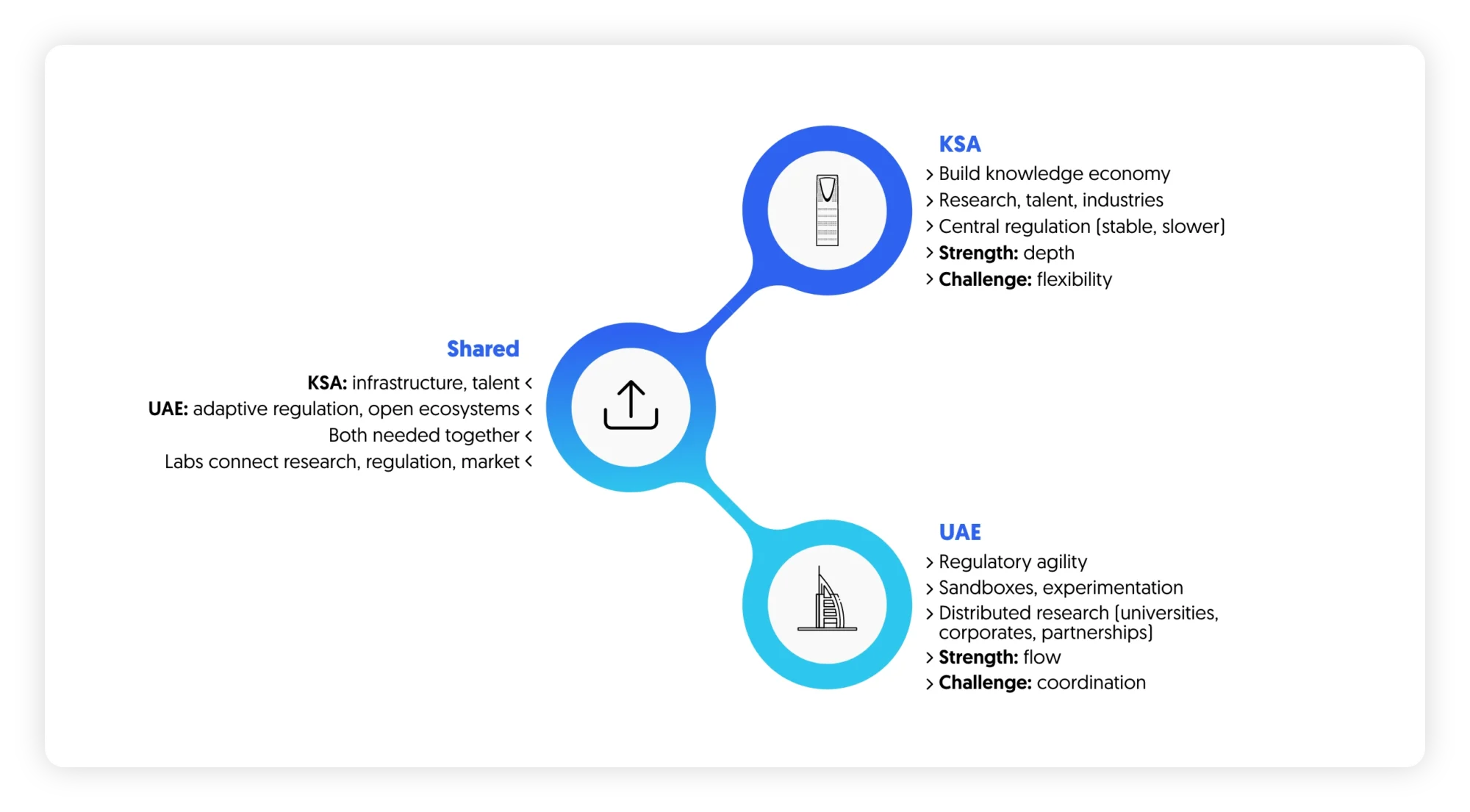

In Saudi Arabia, the emphasis is on constructing the foundations of a knowledge economy at scale.

National programs are being designed to expand research capacity, attract specialized talent, and localize advanced industries. Institutions are being strengthened, new ones are being created, and funding is increasingly directed toward applied research that aligns with priority sectors. Entities like the Saudi Data and AI Authority are not only setting strategy but also shaping how data and AI capabilities are developed and governed across the country.

Regulation, in this context, tends to follow a structured path. Frameworks are defined centrally, often with a focus on stability, security, and alignment with national priorities. This provides clarity at a system level, particularly for large-scale initiatives. At the same time, it can introduce delays when emerging technologies or business models do not fit neatly within existing categories. Adjustments are made, but typically through formal channels that require time and coordination.

The result is a system that is building depth strong institutional backing, clear national direction, and increasing investment in research and talent. The challenge lies in maintaining flexibility as new technologies evolve faster than regulatory cycles.

In the UAE, the balance has tilted more toward regulatory agility.

Authorities have taken a proactive approach to creating environments where new ideas can be tested without waiting for fully developed legislative frameworks. Abu Dhabi Global Market has introduced sandbox models that allow companies to operate under controlled conditions while regulations are refined in parallel. Similarly, initiatives led by the Dubai Future Foundation often combine policy exploration with live experimentation.

Research in the UAE is more distributed. Rather than being concentrated within a few national programs, it is embedded across universities, free zones, corporate R&D centers, and international partnerships. This creates a steady flow of ideas and collaborations, though not always with the same level of central coordination seen in Saudi Arabia.

What emerges from both approaches is a complementary dynamic.

Saudi Arabia is investing heavily in building the infrastructure of innovation institutions, talent pipelines, and sector-specific capabilities. The UAE is refining the mechanisms that allow innovation to move adaptive regulation, open ecosystems, and cross-border integration.

Both are necessary, but neither is sufficient on its own.

Research without pathways to commercialization risks remaining theoretical. Regulation without grounding in real use cases risks becoming either too restrictive or too permissive. Ecosystem development without coordination risks fragmentation.

This is where the interaction between these elements becomes critical.

Innovation does not move in a straight line from research to market. It loops through cycles of testing, validation, and adjustment.

Regulations evolve as edge cases emerge. Research priorities shift based on market feedback. New entrants challenge existing assumptions.

Managing these feedback loops requires environments where experimentation and oversight can coexist.

This is another point where innovation labs begin to play a more strategic role. Not as isolated hubs of creativity, but as interfaces where research can be applied, regulatory assumptions can be tested, and ecosystem actors can align around real-world problems.

Market Scan: Where Innovation Is Impacting the Economy

The impact of innovation in the region is no longer confined to announcements or pilot programs. It is beginning to register in how key sectors are evolving, how capital is being allocated, and how new value is created.

What stands out is not just the range of sectors being targeted, but the way innovation is being used within them. It is less about introducing entirely new industries and more about reconfiguring existing ones to operate differently.

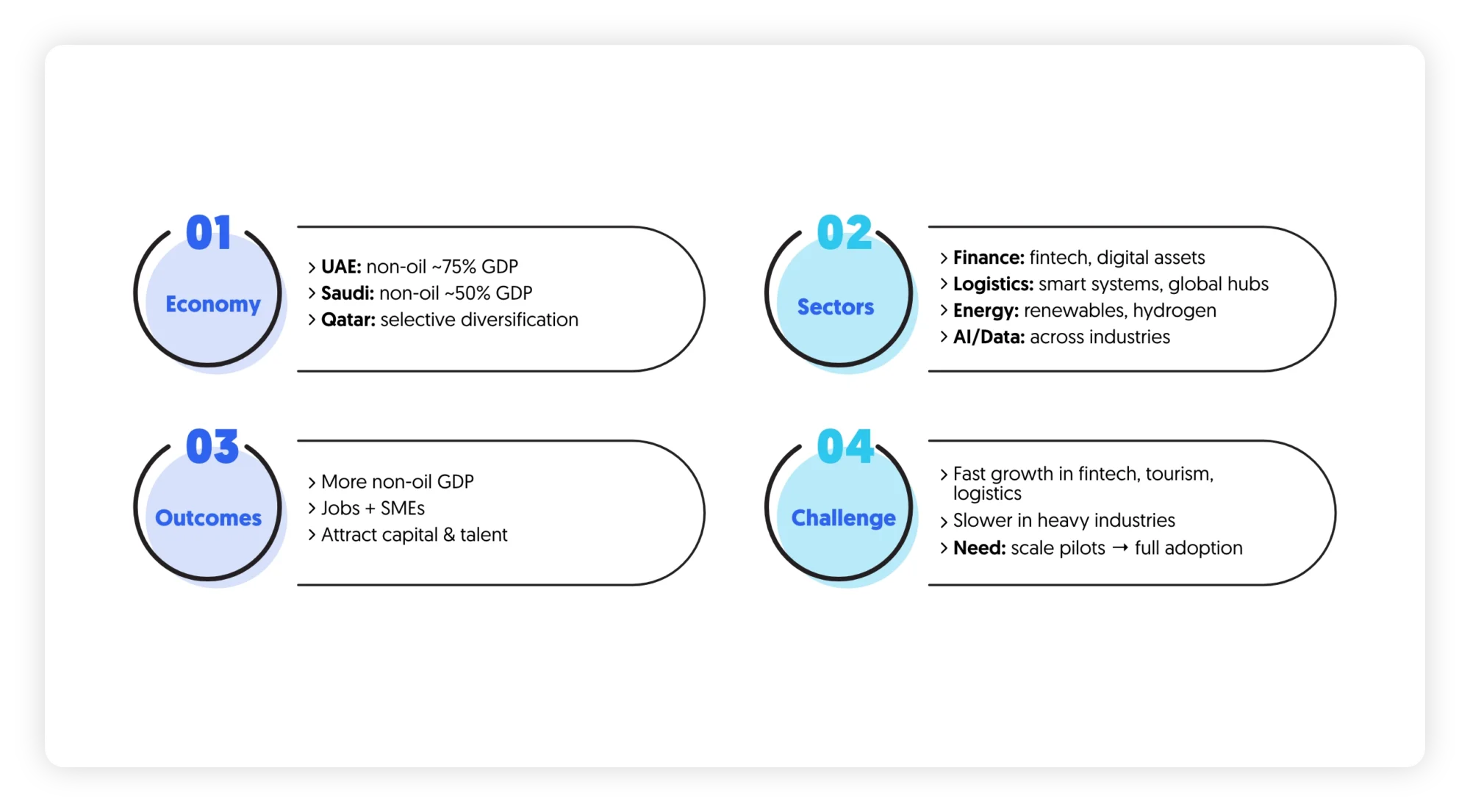

Across the GCC, this shift is already reflected in macroeconomic structure. In the United Arab Emirates, non-oil sectors account for close to three-quarters of GDP, driven by trade, tourism, financial services, and logistics. In Saudi Arabia, the non-oil economy now contributes roughly half of GDP, supported by sustained growth in services, construction, and emerging digital sectors. In Qatar, diversification is more concentrated, with a strong focus on services, energy-adjacent industries, and knowledge-intensive sectors that are gradually increasing their share of output.

These macro shifts are increasingly being shaped by innovation-led transformation across core industries.

In financial services, both Saudi Arabia and the UAE have moved beyond basic digitization. The focus is shifting toward embedded finance, digital assets, and infrastructure-level transformation. The regulatory environment Abu Dhabi Global Market has enabled new models to emerge, while in Saudi Arabia, financial sector transformation programs are driving adoption at scale. The result is a system where traditional banks, fintech startups, and regulators are increasingly interdependent. Fintech alone is now one of the fastest-growing segments in the region, with hundreds of startups operating across payments, lending, and digital banking layers, supported by venture funding that has grown significantly over the past five years.

In mobility and logistics, innovation is tied directly to national competitiveness. Saudi Arabia’s large-scale infrastructure investments part of multi-trillion-dollar transformation programs are being complemented by digital layers such as smart routing, autonomous systems, and integrated logistics platforms. In the UAE, logistics continues to be one of the most advanced ecosystems globally, supported by major infrastructure hubs such as Jebel Ali and increasingly integrated digital trade platforms. Qatar, while smaller in scale, has been investing in logistics and transport infrastructure as part of its broader diversification strategy, particularly around aviation and global connectivity.

Energy is undergoing a more complex transition. The region remains anchored in hydrocarbons, but is actively diversifying into renewables, hydrogen, and energy efficiency technologies. Saudi Arabia and the UAE are among the largest investors in clean energy projects outside the OECD, with multi-billion-dollar commitments to solar, hydrogen, and carbon management systems. Here, innovation is not only technological but also structural reshaping pricing mechanisms, export strategies, and cross-border energy collaboration.

Across these sectors, artificial intelligence and data infrastructure are becoming horizontal enablers rather than standalone domains. Saudi Data and AI Authority are working to standardize and scale data usage across government and industry, while the UAE continues to position itself as a hub for AI deployment and governance. Qatar is also building capability in this space, particularly through research-driven applications in education, energy, and public services.

What ties these developments together is their economic intent.

Innovation is increasingly linked to measurable outcomes: contribution to non-oil GDP, productivity gains, foreign direct investment, and employment creation. In Saudi Arabia, there is a clear push to expand the role of SMEs, which already represent a significant share of private sector activity and are expected to drive future job creation. In the UAE, the emphasis remains on attracting global capital and talent, reinforcing its position as a regional and international hub for business and innovation. Qatar’s approach is more selective, focusing investment into high-impact sectors where long-term economic value can be built through specialization rather than scale.

At the same time, the distribution of impact is uneven.

Certain sectors fintech, logistics, tourism, and government services are advancing quickly, supported by clear use cases and regulatory backing. Tourism alone has become a major economic driver across the region, with Saudi Arabia and the UAE both targeting tens of millions of annual visitors as part of their diversification strategies. Other sectors, particularly those requiring deeper industrial transformation, are progressing more gradually. This reflects not a lack of ambition, but the inherent complexity of rebuilding production systems while maintaining economic stability.

What is becoming evident, however, is that innovation is no longer peripheral to economic growth in the region. It is becoming one of its primary drivers. The next phase will depend less on identifying new opportunities and more on scaling existing ones.

This is where execution, coordination, and the ability to move from pilot to system-wide adoption will define outcomes.

And this is also where many initiatives encounter friction.

Challenges Slowing Down Innovation Impact

As innovation efforts across the region move from early-stage momentum to broader implementation, a different set of constraints begins to surface. These are not about ambition or funding. They are structural, and they tend to appear only once systems are under pressure to deliver at scale.

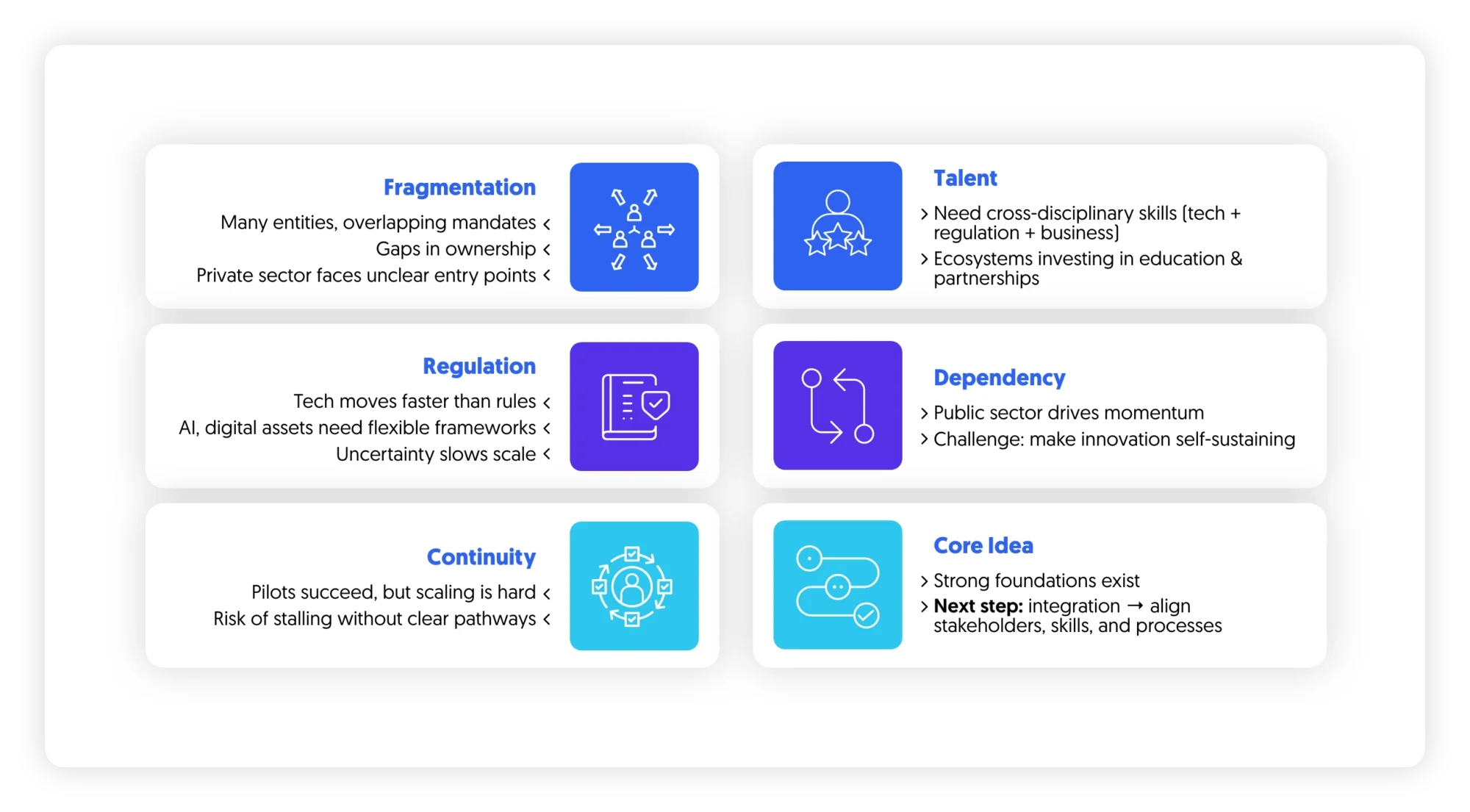

One of the most persistent challenges is fragmentation.

Initiatives are often distributed across multiple entities, each with its own mandate, governance model, and success metrics. While this reflects the breadth of activity in the ecosystem, it also creates overlaps and disconnects. Similar problems are approached in parallel, sometimes with limited visibility across stakeholders. In other cases, gaps emerge where no single entity takes ownership, particularly in cross-sector domains.

For private sector participants, this can translate into unclear entry points. Opportunities exist, but navigating toward them requires time, relationships, and a high tolerance for ambiguity.

A second dimension relates to capability depth, particularly in the development of cross-disciplinary talent.

Rather than a shortage of skills, the region is increasingly focused on expanding profiles that operate across domains technology, regulation, business design, and implementation. This type of capability is becoming more critical as innovation moves closer to execution. The more effective ecosystems in Saudi Arabia, the UAE, and Qatar are already investing in this layer through education systems, industry partnerships, and applied research environments. The direction of travel is clear: innovation capacity is increasingly defined by the ability to connect disciplines rather than operate within them in isolation.

Regulation presents another layer of complexity.

While Saudi Arabia and the UAE have made significant strides in modernizing regulatory frameworks, the pace of technological change continues to outstrip formal processes. Emerging areas such as AI, digital assets, and advanced manufacturing often require iterative approaches to regulation. In practice, this means uncertainty can persist longer than organizations anticipate. Some stakeholders choose to wait for clarity; others move forward and adjust in real time. Neither approach is fully efficient at scale, particularly in fast-moving sectors.

There is also a structural dependency on government-led momentum.

Public sector entities remain the primary drivers of large innovation initiatives, particularly in Saudi Arabia, where national programs set direction and unlock scale. This has clear advantages in terms of coordination and funding. However, in all three models Saudi Arabia, the UAE, and Qatar the longer-term challenge is similar: ensuring that innovation activity becomes self-sustaining beyond initial public sector stimulus. Private sector participation tends to increase when demand is predictable, pathways to scale are visible, and regulatory conditions are stable enough to support long-term investment.

Finally, there is the question of continuity.

Many innovation initiatives begin as pilots or standalone programs. They generate insights, demonstrate potential, and sometimes achieve early success. The challenge comes in what follows. Transitioning from pilot to full-scale implementation often requires different capabilities, governance structures, and levels of ownership across stakeholders. Without a clear pathway, initiatives risk stalling at the point where they should be expanding.

Taken together, these challenges point to a common theme.

Across Saudi Arabia, the UAE, and Qatar, strong foundations for innovation are in place. The next hurdle is integration aligning stakeholders, capabilities, and processes in a way that allows ideas to move consistently from concept to impact.

This is not a problem that can be solved through additional funding or high-level strategy alone. It requires mechanisms that operate within the system, addressing friction as it arises and enabling progress across institutional boundaries.

Which brings the focus back to how these mechanisms are designed and deployed in practice.

Where Innovation Labs Fit

By this stage, the role of innovation labs becomes less conceptual and more operational. The question is no longer what they are, but how they are positioned within the system and whether they are designed to address the specific frictions outlined earlier.

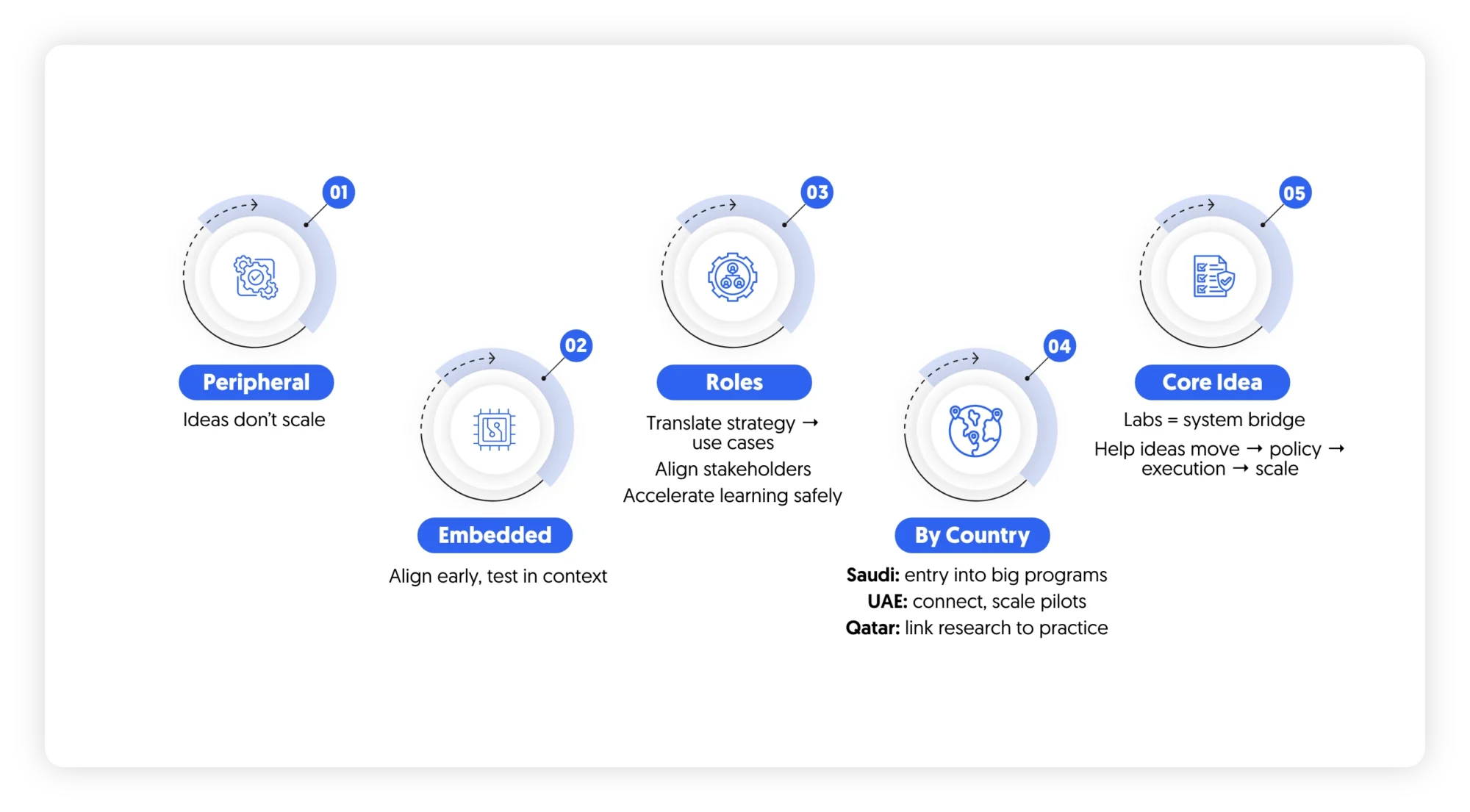

Many organizations in the region already have some form of “innovation function.” The distinction lies in whether that function is peripheral or embedded.

When labs operate at the edges separated from decision-making, disconnected from live initiatives they tend to produce outputs that are difficult to integrate. Concepts are developed, prototypes are built, but adoption depends on external stakeholders who were not part of the process. Momentum slows, not because of lack of quality, but because alignment was never established.

In contrast, labs that are positioned closer to core operations behave differently.

They are involved early, often at the stage where problems are still being defined. They work alongside policy teams, business units, and external partners to shape the scope of initiatives before significant resources are committed. This changes the nature of their output. Instead of abstract ideas, they produce validated directions options that have already been tested against regulatory constraints, user needs, and operational realities.

This positioning allows innovation labs to play three distinct roles.

First, they act as a translation layer. Strategies articulated at a national or organizational level are often broad by design. Turning them into executable initiatives requires interpretation. Labs break these strategies down into specific use cases, identify where value can be created, and clarify what needs to be true for implementation to succeed.

Second, they function as an alignment mechanism. By bringing together stakeholders government entities, corporates, startups, regulators within a structured environment, labs create a shared understanding of both the problem and the solution space. This reduces the risk of divergence later in the process, when alignment becomes more costly to achieve.

Third, they serve as an acceleration layer, but in a controlled sense. Rather than pushing for speed at all costs, they compress learning cycles. Assumptions are tested early, feedback is incorporated quickly, and decisions are made based on evidence rather than projections. This shortens the path from concept to implementation without bypassing necessary safeguards.

For organizations operating across Saudi Arabia, the UAE, and Qatar, this model has different but complementary implications.

In Saudi Arabia’s centralized environment, innovation labs help structure entry points into large national initiatives, ensuring that external participation is aligned with system-wide priorities.

In the UAE’s distributed ecosystem, they reduce fragmentation by connecting actors across sectors, enabling successful pilots to scale beyond localized environments.

In Qatar’s more focused, research-led model, labs reinforce the link between experimentation and applied knowledge, ensuring that innovation efforts remain tightly connected to long-term capability building and targeted national priorities.

The underlying principle is consistent across all three contexts.

Innovation labs are most effective when they are not treated as standalone entities, but as part of the system’s operating model. Their value lies less in generating ideas and more in ensuring that ideas can travel across institutions, from policy to execution, and from pilot to scale.

Across the Gulf, innovation is no longer defined by the presence of strategy or the scale of investment. It is increasingly defined by how effectively systems can move from intent to execution. Saudi Arabia is building depth at scale, the UAE is enabling flow across ecosystems, and Qatar is reinforcing targeted capability through focused, research-driven development. Different models, but a shared constraint: the need to connect ambition with implementation. Innovation labs sit at that intersection not as innovation spaces, but as operational mechanisms that determine whether transformation efforts translate into sustained economic impact.