Blockchain technology has gained significant attention in recent years, primarily due to its association with cryptocurrencies like Bitcoin. However, its applications extend far beyond digital currencies, offering transformative potential across various industries, particularly in enhancing customer experience.

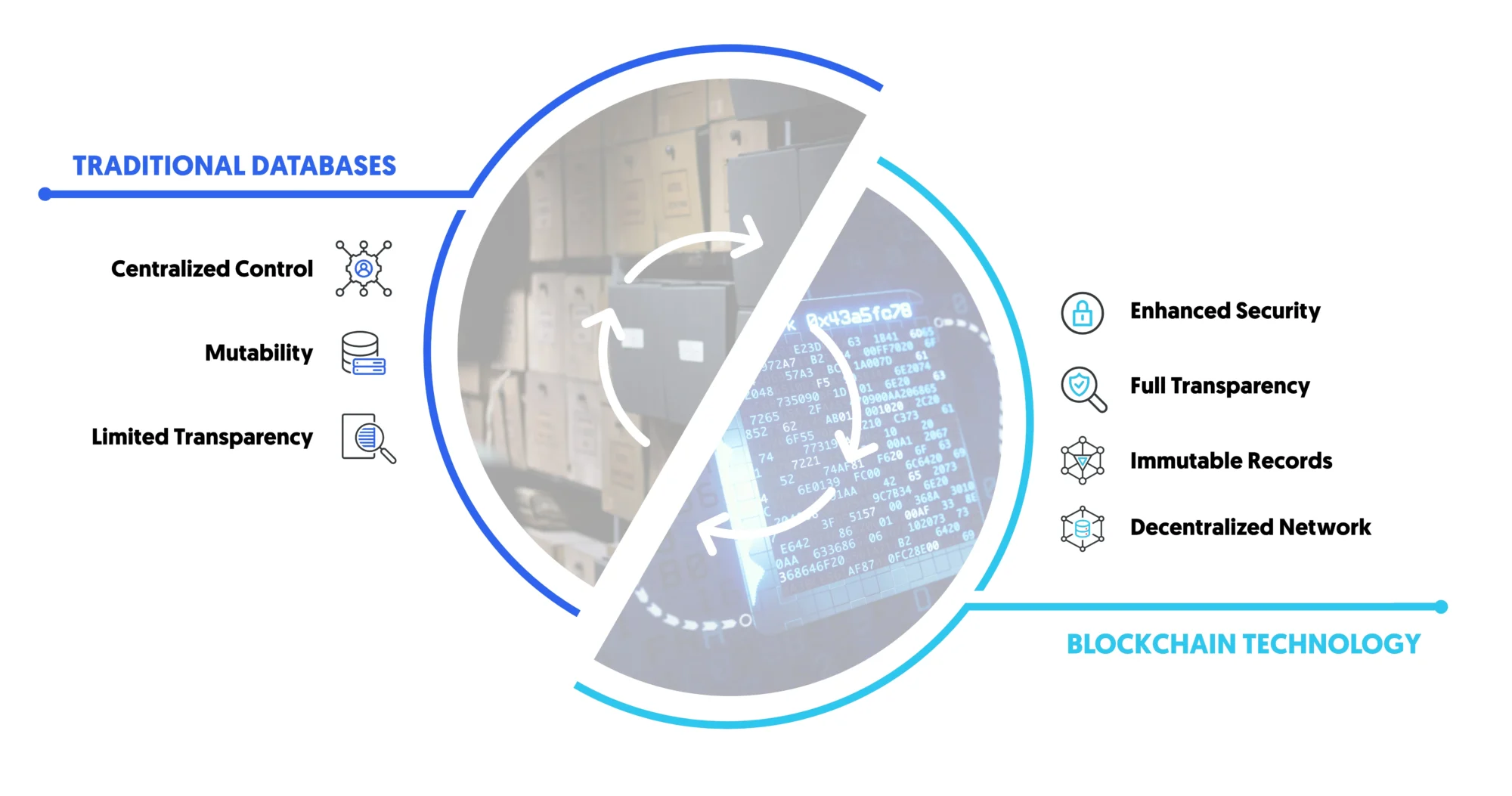

Blockchain vs. Traditional Databases

Blockchain is a distributed ledger technology that enables secure, transparent, and tamper-proof recording of transactions across a network of computers. Unlike traditional centralized systems, blockchain operates on a decentralized network, meaning no single entity has control over the entire database.

Traditional Databases

- Centralized Control: Traditional databases are typically managed by a single central authority, which controls the entire system. This centralization can create vulnerabilities, as the database becomes a single point of failure.

- Mutability: In traditional databases, data can be modified or deleted by those with sufficient access rights. While this allows for flexibility, it also raises concerns about data integrity and security.

- Limited Transparency: Access to traditional databases is usually restricted, and not all participants can view the complete transaction history. This lack of transparency can lead to mistrust and discrepancies in data.

Blockchain Technology

- Decentralized Network: Blockchain operates on a peer-to-peer network where multiple nodes maintain and validate the ledger. This decentralization enhances security and resilience.

- Immutable Records: Once data is recorded on the blockchain, it cannot be changed or deleted. This immutability ensures the integrity and permanence of transaction records.

- Full Transparency: All transactions on the blockchain are visible to all network participants, providing a transparent and verifiable history of data. This transparency builds trust and accountability.

- Enhanced Security: Blockchain uses cryptographic techniques to secure transactions, making it highly resistant to hacking and fraud.

Enhancing Data Security and Privacy

Blockchain technology with its decentralized nature and advanced encryption mechanisms provide a secure environment for transactions and data storage, which is crucial for maintaining customer trust.

Secure Transactions

Encryption and Decentralization

- Cryptographic Security: Blockchain uses advanced cryptographic techniques to secure data. Each transaction is encrypted and linked to the previous transaction, creating a chain of secure blocks. This encryption ensures that data is protected from unauthorized access and tampering.

- Decentralized Validation: In a blockchain network, transactions are validated by a distributed network of nodes rather than a single central authority. This decentralized validation process, often achieved through consensus mechanisms like Proof of Work (PoW) or Proof of Stake (PoS), makes it extremely difficult for any single entity to alter transaction data.

Protection Against Breaches and Fraud

- Immutable Ledger: Once a transaction is recorded on the blockchain, it cannot be altered or deleted. This immutability ensures that historical transaction data remains accurate and tamper-proof, providing a reliable audit trail.

- Reduced Single Points of Failure: Unlike traditional centralized systems, where a single point of failure can compromise the entire system, blockchain’s decentralized nature distributes the risk across multiple nodes. This distribution enhances security by reducing the likelihood of successful cyberattacks.

- Fraud Prevention: Blockchain’s transparent and immutable ledger makes it easier to detect and prevent fraudulent activities. Every transaction is recorded and visible to all participants, making it nearly impossible to commit fraud without detection.

Data Privacy

Customer Control Over Personal Data

- Self-Sovereign Identity: Blockchain technology supports the concept of self-sovereign identity, where individuals have control over their personal data. Customers can store their identity and personal information on the blockchain and control who has access to it.

- Permissioned Access: Blockchain allows customers to grant permission to specific entities to access their data. This permissioned access ensures that only authorized parties can view or use personal information, enhancing privacy.

Transparent and Verifiable Access

- Access Logs: Every access request and transaction involving personal data is recorded on the blockchain. These access logs are transparent and immutable, allowing customers to verify who has accessed their data and when.

- Selective Disclosure: Blockchain enables selective disclosure, where customers can share only the necessary pieces of information without revealing their entire identity. For example, they can prove their age without disclosing their date of birth.

Enhanced Privacy Mechanisms

- Zero-Knowledge Proofs: Advanced cryptographic techniques like zero-knowledge proofs (ZKPs) allow customers to prove the validity of certain information without revealing the actual data. This mechanism can be used to enhance privacy in various applications, such as verifying credentials or financial transactions.

- Decentralized Storage: Blockchain can be used in conjunction with decentralized storage solutions to further enhance data privacy. By distributing data across a decentralized network, the risk of data breaches is minimized, and customers retain greater control over their information.

Regulatory Compliance

- GDPR and CCPA: Blockchain can help businesses comply with data privacy regulations such as the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA). By giving customers control over their data and ensuring transparent access logs, blockchain aligns with the principles of data protection and privacy outlined in these regulations.

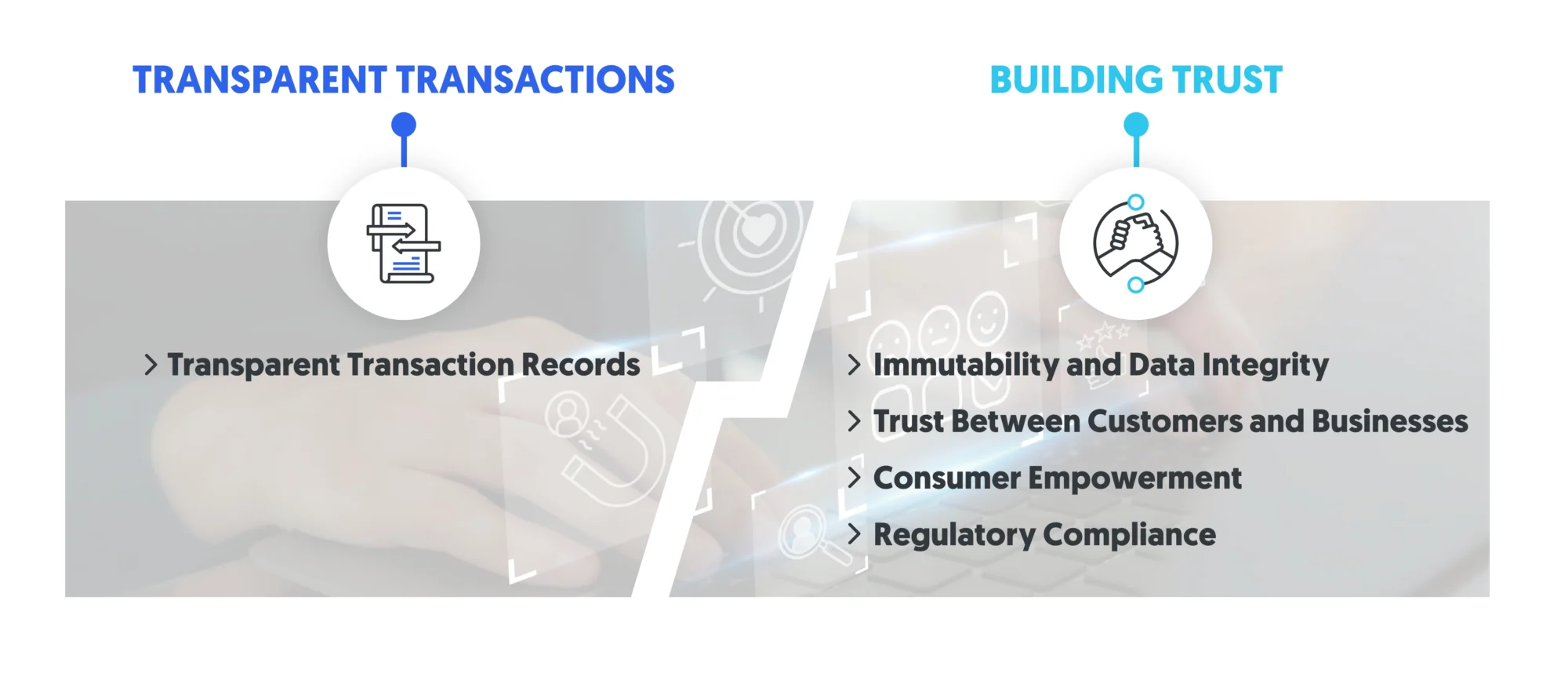

Improving Transparency and Trust

Blockchain technology significantly enhances transparency and trust between businesses and customers.

Transparent Transactions

Transparent Transaction Records

- Public Ledger: Blockchain operates as a public ledger where every transaction is recorded and accessible to all network participants. This transparency allows customers to verify the details of transactions independently.

- Traceability: Each transaction on the blockchain is timestamped and linked to the previous one, creating a chronological chain of events. This traceability is particularly valuable in supply chain management, where customers can track the journey of a product from origin to delivery.

- Verification of Authenticity: Customers can use blockchain to verify the authenticity of products and services. For instance, in the case of luxury goods or pharmaceuticals, blockchain can provide a verifiable history of the product’s origin, manufacturing process, and distribution chain. This ensures that customers are purchasing genuine products.

In the food industry, blockchain can be used to provide transparency from farm to table. Each step of the food production process, from harvesting to packaging and shipping, can be recorded on the blockchain. Consumers can scan a QR code on the product to access its entire history, ensuring that it meets quality and safety standards.

Building Trust

Immutability and Data Integrity

- Immutable Records: Once a transaction is recorded on the blockchain, it cannot be altered or deleted. This immutability ensures that the transaction history remains accurate and tamper-proof, which is crucial for maintaining data integrity.

- Data Authenticity: Blockchain’s immutable nature guarantees that the data recorded is authentic and has not been manipulated. This builds trust among customers, as they can be confident that the information they are accessing is reliable.

Trust Between Customers and Businesses

- Enhanced Accountability: Businesses that adopt blockchain technology demonstrate a commitment to transparency and accountability. By providing customers with access to verifiable transaction records, businesses can build a reputation for honesty and integrity.

- Conflict Resolution: In cases of disputes or claims, blockchain’s transparent and immutable records provide a clear and verifiable source of truth. This can expedite conflict resolution and ensure fair outcomes based on accurate data.

The diamond industry faces challenges related to the authenticity and ethical sourcing of diamonds. Blockchain can be used to track the journey of each diamond from the mine to the retailer, ensuring that it is conflict-free and ethically sourced. Customers can verify the diamond’s origin and history, building trust in the product and the brand.

Consumer Empowerment

- Informed Decisions: By providing transparent access to transaction data, blockchain empowers consumers to make informed decisions. They can verify product claims, assess the quality and origin of goods, and choose brands that align with their values.

- Building Loyalty: When customers trust a brand and feel confident in the authenticity and quality of its products, they are more likely to remain loyal. Blockchain helps build this trust, fostering long-term customer relationships.

Regulatory Compliance

- Adhering to Standards: Blockchain’s transparency and immutability can also help businesses comply with regulatory standards and demonstrate adherence to industry regulations. This further enhances trust among customers who seek assurance that products and services meet legal and ethical standards.

Streamlining Processes and Reducing Costs

Blockchain technology offers transformative potential for streamlining processes and reducing costs across various industries.

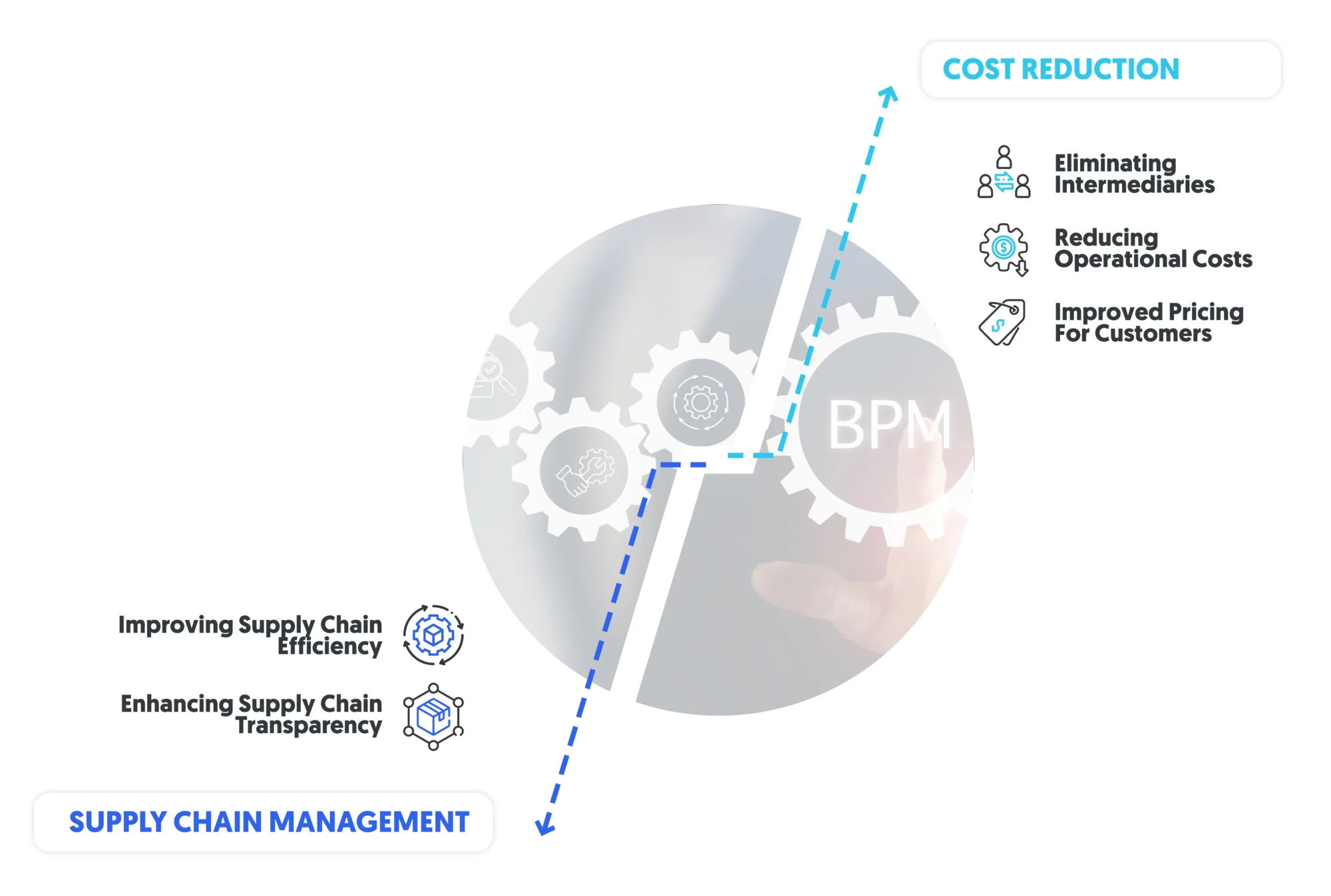

Supply Chain Management

Enhancing Supply Chain Transparency

- End-to-End Visibility: Blockchain provides a transparent and immutable record of each transaction in the supply chain. This end-to-end visibility allows all participants, including customers, to track products from their origin to the final delivery point. Each step, from raw material sourcing to manufacturing and shipping, is recorded on the blockchain, providing a comprehensive view of the product’s journey.

- Verification of Authenticity: Customers can use blockchain to verify the authenticity of products. For example, in industries like pharmaceuticals and luxury goods, blockchain can ensure that products are genuine and not counterfeit. By scanning a QR code, customers can access detailed information about the product’s history and verify its authenticity.

Improving Supply Chain Efficiency

- Real-Time Tracking: Blockchain enables real-time tracking of products, allowing businesses to monitor the status and location of shipments at any time. This real-time data can help optimize inventory management, reduce delays, and improve overall supply chain efficiency.

- Automated Processes with Smart Contracts: Smart contracts, which are self-executing contracts with the terms of the agreement directly written into code, can automate various processes within the supply chain. For instance, payments can be automatically triggered once a shipment is received, reducing administrative overhead and speeding up transactions.

- Reducing Errors and Fraud: Blockchain’s immutable and transparent nature reduces the risk of errors and fraud in the supply chain. Each transaction is verified and recorded on the blockchain, making it difficult to alter records or commit fraudulent activities.

In the food industry, blockchain can be used to quickly trace the source of contaminated products. If a foodborne illness outbreak occurs, blockchain can help identify the origin of the contaminated batch and track its distribution path. This rapid traceability can help contain the spread of the contamination and ensure the safety of consumers.

Cost Reduction

Eliminating Intermediaries

- Direct Transactions: Blockchain enables direct transactions between parties without the need for intermediaries. This can significantly reduce transaction costs associated with third-party fees and commissions. For example, in the financial industry, blockchain can facilitate direct cross-border payments, eliminating the need for banks and payment processors.

- Streamlined Processes: By automating processes with smart contracts, blockchain reduces the need for manual intervention and administrative tasks. This streamlining of operations leads to cost savings in terms of labor and time.

Reducing Operational Costs

- Efficient Record Keeping: Blockchain’s decentralized and transparent nature simplifies record keeping and reduces the need for extensive paperwork and manual reconciliations. This efficiency reduces operational costs and minimizes the risk of errors.

- Supply Chain Optimization: Real-time tracking and data visibility provided by blockchain can help businesses optimize their supply chains. By having accurate and timely information, companies can better manage inventory levels, reduce waste, and avoid overstocking or stockouts.

Improved Pricing for Customers

- Cost Savings Passed to Customers: The cost savings achieved through blockchain’s efficiency and reduced need for intermediaries can be passed on to customers in the form of better pricing. Lower transaction and operational costs allow businesses to offer more competitive prices, enhancing customer satisfaction.

- Increased Trust and Loyalty: By providing transparent and verifiable information about product authenticity and supply chain practices, businesses can build trust and loyalty among customers. This trust can lead to increased sales and customer retention, further contributing to cost efficiencies and competitive pricing.

In international trade, cross-border payments often involve multiple banks and intermediaries, leading to high fees and long processing times. Blockchain can streamline this process by enabling direct peer-to-peer transactions, reducing fees, and speeding up settlement times. This efficiency benefits both businesses and customers, who enjoy faster and more cost-effective transactions.

Enhancing Loyalty Programs and Rewards

Blockchain technology offers innovative solutions for improving loyalty programs and rewards, providing security, transparency, and increased flexibility for customers.

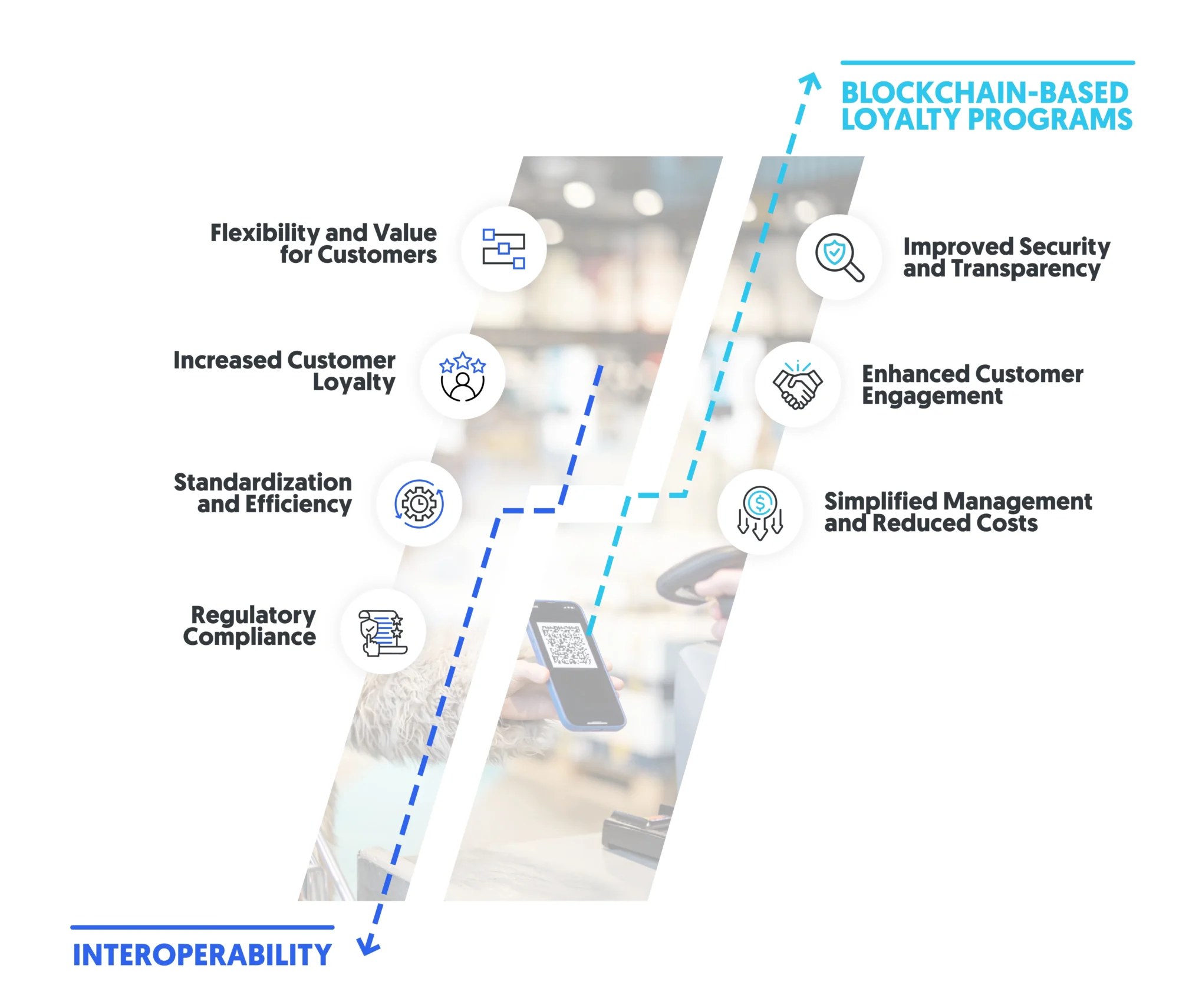

Blockchain-Based Loyalty Programs

Improved Security and Transparency

- Secure Issuance and Tracking: Blockchain provides a secure and transparent platform for issuing and tracking loyalty points or rewards. Each transaction involving loyalty points is recorded on the blockchain, ensuring that points cannot be duplicated or fraudulently manipulated. This security helps maintain the integrity of the loyalty program and protects it from abuse.

- Immutable Records: The immutable nature of blockchain ensures that all transactions are permanently recorded and cannot be altered. This provides a reliable and verifiable history of all loyalty points issued and redeemed, building trust between the business and its customers.

Enhanced Customer Engagement

- Real-Time Updates: Blockchain enables real-time updates to loyalty point balances and rewards. Customers can instantly see their updated point balance and redeem rewards without delays. This immediate feedback enhances the customer experience and encourages continued participation in the loyalty program.

- Personalized Rewards: With the transparent and secure nature of blockchain, businesses can offer personalized rewards based on customer preferences and behaviors. By analyzing transaction data, businesses can tailor rewards to individual customers, increasing their engagement and satisfaction.

Simplified Management and Reduced Costs

- Streamlined Administration: Blockchain automates the issuance and redemption of loyalty points, reducing the administrative burden on businesses. Smart contracts can be used to automate these processes, ensuring that points are accurately and efficiently managed.

- Cost Savings: By eliminating intermediaries and reducing the complexity of managing loyalty programs, blockchain can lower operational costs. These savings can be passed on to customers through better rewards or more competitive pricing.

Blockchain can be used to manage frequent flyer points, ensuring that points are securely issued and accurately tracked. Customers can easily transfer points between different airline partners, enhancing their ability to earn and redeem rewards across a wider network.

Interoperability

Flexibility and Value for Customers

- Unified Loyalty Programs: Blockchain allows for the creation of unified loyalty programs that span multiple businesses or brands. Customers can earn and redeem points across a network of participating companies, providing greater flexibility and value. For example, a customer could use points earned at a retail store to get a discount at a restaurant.

- Seamless Integration: Blockchain’s decentralized nature facilitates seamless integration between different loyalty programs. Businesses can collaborate on a common blockchain platform, allowing customers to transfer and use points across various programs without any friction.

Increased Customer Loyalty

- Broader Reward Options: By offering a wider range of reward options through interoperable loyalty programs, businesses can increase customer satisfaction and loyalty. Customers are more likely to engage with programs that offer versatile and valuable rewards.

- Enhanced Customer Experience: The ability to easily combine and use loyalty points from different programs enhances the overall customer experience. Customers appreciate the convenience and flexibility of using their points in a way that best suits their needs.

A blockchain-based loyalty program could enable customers to earn points at a retail store and redeem them at a partnering hotel chain. This cross-industry collaboration increases the appeal of both loyalty programs, as customers benefit from a broader range of rewards.

Standardization and Efficiency

- Common Standards: Blockchain can help establish common standards for loyalty programs, ensuring interoperability and consistency across different businesses. This standardization simplifies the customer experience and makes it easier for businesses to collaborate.

- Efficient Management: With interoperable blockchain-based loyalty programs, businesses can manage loyalty points more efficiently. The shared ledger provides a single source of truth for all transactions, reducing the risk of errors and discrepancies.

Regulatory Compliance

- Transparent Reporting: Blockchain’s transparent nature ensures that all transactions involving loyalty points are accurately recorded and easily auditable. This transparency helps businesses comply with regulatory requirements and provides customers with confidence in the program’s integrity.

Facilitating Seamless and Secure Payments

Blockchain technology has the potential to revolutionize payment systems by offering more secure, efficient, and cost-effective solutions.

Benefits of Accepting Cryptocurrency Payments

- Lower Transaction Fees: Traditional payment methods often involve high transaction fees due to intermediaries like banks and payment processors. Cryptocurrencies can drastically reduce these fees by eliminating intermediaries and enabling peer-to-peer transactions. This cost-saving can be beneficial for both businesses and customers.

- Faster Transaction Times: Cryptocurrency transactions are typically faster than traditional payment methods. While bank transfers can take several days to settle, cryptocurrency transactions can be completed within minutes, providing a quicker and more efficient payment process.

- Global Accessibility: Cryptocurrencies are accessible to anyone with an internet connection, regardless of their location. This global accessibility allows businesses to reach a broader customer base and facilitates international transactions without the need for currency conversions.

- Enhanced Security: Cryptocurrencies use advanced cryptographic techniques to secure transactions. Each transaction is verified and recorded on the blockchain, making it difficult for fraudsters to manipulate or counterfeit transactions.

- Transparency and Immutability: All cryptocurrency transactions are recorded on a public ledger, ensuring transparency and immutability. Customers and businesses can verify transactions independently, fostering trust in the payment system.

Many e-commerce platforms now accept Bitcoin and other cryptocurrencies as payment. This acceptance allows customers to make purchases quickly and securely, while businesses benefit from lower transaction fees and the ability to attract tech-savvy customers.

Simplifying and Securing Cross-Border Transactions

- Eliminating Intermediaries: Traditional cross-border transactions often involve multiple banks and financial intermediaries, leading to delays and high fees. Blockchain simplifies this process by enabling direct peer-to-peer transactions, reducing the need for intermediaries and lowering costs.

- Faster Settlements: Cross-border payments through blockchain can be processed much faster than traditional methods. Instead of waiting several days for a bank transfer to clear, blockchain transactions can settle within minutes, providing a more efficient payment experience for international purchases.

- Reduced Currency Conversion Fees: Blockchain-based payments can reduce or eliminate currency conversion fees. Customers can pay with their preferred cryptocurrency, and businesses can choose to receive payments in their desired currency or cryptocurrency, reducing the costs associated with currency exchange.

- Enhanced Security and Fraud Prevention: Blockchain’s decentralized and transparent nature enhances the security of cross-border transactions. Each transaction is cryptographically secured and recorded on the blockchain, making it nearly impossible to alter or counterfeit. This reduces the risk of fraud and enhances the overall security of international transactions.

Blockchain can be particularly beneficial for remittances, where individuals send money across borders to family members. Traditional remittance services can be expensive and slow, but blockchain-based services offer faster and cheaper alternatives. For example, companies like Ripple use blockchain technology to enable quick and cost-effective cross-border payments.

Enhancing Customer Experience

- Transparency and Traceability: Blockchain provides complete transparency and traceability of transactions. Customers can track their payments in real-time, knowing exactly where their money is at any given moment. This transparency builds trust and enhances the customer experience.

- Access to New Markets: By facilitating seamless and secure cross-border transactions, blockchain opens up new markets for businesses. Customers from different parts of the world can easily purchase products and services, expanding the customer base and increasing revenue opportunities for businesses.

- Compliance and Reporting: Blockchain’s transparent ledger makes it easier for businesses to comply with regulatory requirements and generate accurate reports. This compliance ensures that cross-border transactions meet legal standards, providing peace of mind for both businesses and customers.

In international trade, blockchain can streamline trade finance processes by reducing paperwork and ensuring the accuracy of transaction records. Smart contracts can automate payment and delivery terms, reducing delays and enhancing the efficiency of cross-border trade.

Challenges and Considerations

While blockchain technology offers numerous benefits for enhancing customer experience, businesses must also navigate several challenges and considerations. These include scalability issues, regulatory and compliance hurdles, and adoption barriers.

Scalability Issues

Current Limitations

- Transaction Speed: One of the primary challenges of blockchain technology is transaction speed. Popular blockchain networks, such as Bitcoin and Ethereum, can process only a limited number of transactions per second (TPS). For example, Bitcoin processes around 7 TPS, while Ethereum handles about 30 TPS. This limitation makes it difficult for blockchain to support large-scale applications with high transaction volumes.

- Network Congestion: As the number of users and transactions on a blockchain network increases, the network can become congested. This congestion leads to slower transaction times and higher transaction fees, which can negatively impact the user experience.

- Scalability Solutions: Various solutions are being explored to address scalability issues. Layer 2 solutions, such as the Lightning Network for Bitcoin and Plasma for Ethereum, aim to process transactions off-chain while settling them on-chain. Sharding, another technique, divides the blockchain into smaller, more manageable pieces, each capable of processing transactions independently.

The popular blockchain-based game CryptoKitties highlighted scalability issues when it launched on the Ethereum network in 2017. The game’s popularity led to significant network congestion, slowing down transactions and increasing fees for all Ethereum users.

Regulations and Compliance

Regulatory Challenges

- Uncertain Legal Frameworks: The regulatory landscape for blockchain and cryptocurrencies is still evolving. Different countries have varying approaches to regulating blockchain technology, leading to uncertainty for businesses operating in multiple jurisdictions. Some governments have embraced blockchain, while others have imposed strict regulations or outright bans.

- Compliance Requirements: Businesses using blockchain technology must comply with existing regulations related to data privacy, financial transactions, and anti-money laundering (AML). Compliance can be challenging due to the decentralized and pseudonymous nature of blockchain transactions.

Data Privacy and GDPR

- Right to Erasure: The General Data Protection Regulation (GDPR) in the European Union grants individuals the right to have their personal data erased. However, blockchain’s immutable nature makes it difficult to delete data once it is recorded on the blockchain. Businesses must find ways to balance blockchain’s transparency with data privacy requirements.

ICOs, a popular method for blockchain startups to raise funds, have faced regulatory scrutiny due to concerns about fraud and investor protection. Regulatory bodies like the U.S. Securities and Exchange Commission (SEC) have taken action against ICOs that violate securities laws, highlighting the need for compliance in blockchain projects.

Adoption Barriers

Technological Integration

- Complex Integration: Integrating blockchain technology into existing systems can be complex and resource-intensive. Businesses may need to invest in new infrastructure, train employees, and develop new processes to leverage blockchain effectively.

- Interoperability Issues: Different blockchain platforms may not be compatible with one another, creating interoperability challenges. Businesses must ensure that their blockchain solutions can communicate with other systems and platforms to maximize their benefits.

Customer Acceptance

- Understanding and Trust: Customers may be unfamiliar with blockchain technology and hesitant to trust it for transactions and data management. Educating customers about the benefits and security features of blockchain is crucial for gaining their acceptance.

- User Experience: The user experience of blockchain applications can be less intuitive than traditional applications. Businesses must focus on designing user-friendly interfaces to encourage adoption and usage.

A major retail company looking to implement blockchain for supply chain transparency must integrate the technology with its existing inventory management and logistics systems. This integration requires significant investment and coordination across multiple departments.

Financial and Resource Constraints

- Investment Costs: Implementing blockchain technology can require substantial financial investment, particularly for small and medium-sized enterprises (SMEs). Businesses need to assess the return on investment (ROI) and ensure that the benefits outweigh the costs.

- Resource Allocation: Developing and maintaining blockchain solutions requires specialized skills and resources. Businesses may need to hire or train personnel with expertise in blockchain technology, which can be a challenge given the current talent shortage in this field.

A small business interested in using blockchain for secure payments might face challenges in allocating resources for development and integration. The business must carefully evaluate the costs and benefits to determine if blockchain is a viable solution.

Future Trends and Innovations

Blockchain technology is continuously evolving, and its integration with other emerging technologies, such as Artificial Intelligence (AI) and the Internet of Things (IoT), promises to further enhance customer experience. Understanding these future trends and innovations can help businesses stay ahead of the curve and leverage blockchain for competitive advantage.

Emerging Technologies

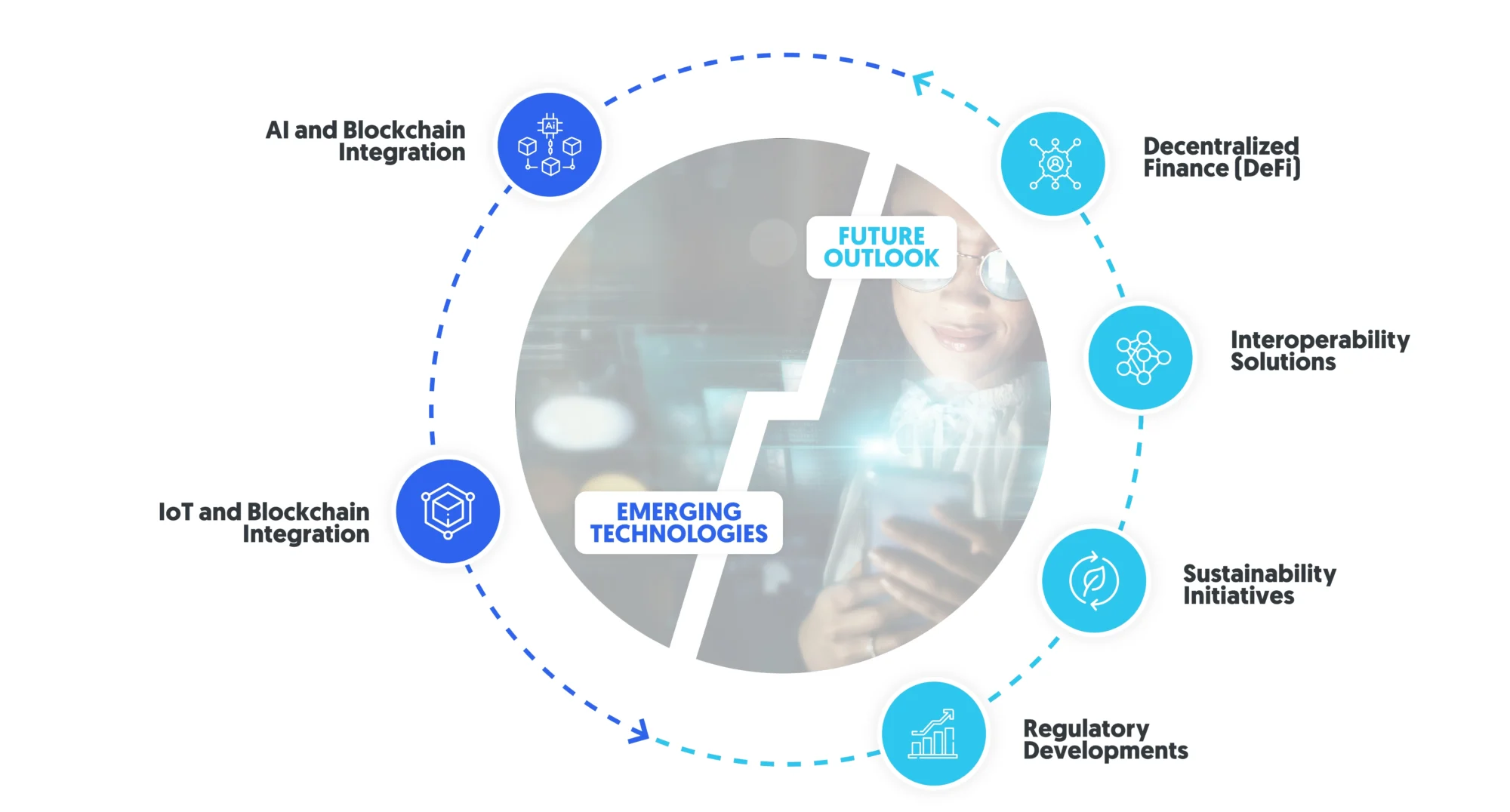

AI and Blockchain Integration

- Enhanced Data Analytics: AI can analyze the vast amounts of data stored on the blockchain to derive valuable insights. For example, AI algorithms can detect patterns in customer behavior, helping businesses to tailor their products and services to meet customer needs more effectively. This integration can lead to more personalized customer experiences and improved satisfaction.

- Automated Smart Contracts: Combining AI with blockchain’s smart contracts can automate complex processes and decision-making. AI can trigger smart contracts based on predefined criteria and real-time data analysis, ensuring seamless execution of transactions and agreements without human intervention. This automation enhances efficiency and reduces the risk of errors.

- Predictive Maintenance: In industries like manufacturing and supply chain management, AI can predict equipment failures and maintenance needs based on data recorded on the blockchain. This proactive approach minimizes downtime and ensures smoother operations, ultimately improving the customer experience by ensuring timely deliveries and high-quality products.

IoT and Blockchain Integration

- Secure Device Communication: Blockchain can provide a secure and transparent framework for IoT devices to communicate and transact. Each device can have a unique identity on the blockchain, ensuring that all interactions are authenticated and tamper-proof. This security is crucial for applications like smart homes and connected vehicles, where data integrity is paramount.

- Supply Chain Visibility: IoT devices can track products throughout the supply chain and record data on the blockchain. Sensors can monitor conditions such as temperature, humidity, and location, providing real-time visibility into the status of goods. This transparency ensures that customers receive high-quality products and can trace the journey of their purchases.

- Automated Transactions: IoT devices can autonomously execute transactions using blockchain. For example, a connected refrigerator could automatically reorder groceries when supplies run low, with payments securely processed via blockchain. This convenience enhances the customer experience by simplifying everyday tasks.

A logistics company can use IoT sensors to monitor the condition and location of shipments in real-time. The data is recorded on the blockchain, providing an immutable and transparent record of the shipment’s journey. AI algorithms can analyze this data to optimize routes and predict delivery times, ensuring that customers receive their orders promptly and in good condition.

Future Outlook

Decentralized Finance (DeFi)

- Financial Inclusion: DeFi leverages blockchain to provide financial services without traditional intermediaries like banks. This innovation can increase financial inclusion by offering accessible and affordable services to underserved populations. Customers can benefit from decentralized lending, borrowing, and investment platforms that operate transparently and securely.

- Tokenization of Assets: DeFi enables the tokenization of real-world assets, such as real estate, art, and commodities. Customers can invest in fractional ownership of these assets, enhancing liquidity and democratizing access to investment opportunities. Tokenized assets are easily tradable on blockchain platforms, providing greater flexibility and convenience.

Interoperability Solutions

- Cross-Chain Communication: Future developments in blockchain interoperability will enable seamless communication between different blockchain networks. This cross-chain communication allows for the transfer of assets and data across multiple platforms, enhancing the flexibility and utility of blockchain applications. Customers can benefit from more comprehensive services that leverage the strengths of different blockchains.

- Unified User Experience: Interoperability solutions will create a more unified user experience, where customers can interact with various blockchain-based services through a single interface. This convenience reduces complexity and makes blockchain technology more accessible to a broader audience.

Sustainability Initiatives

- Green Blockchain Technologies: As environmental concerns grow, there is a push for more sustainable blockchain technologies. Innovations such as Proof-of-Stake (PoS) and energy-efficient consensus mechanisms are being developed to reduce the carbon footprint of blockchain operations. Customers increasingly value sustainability, and businesses that adopt green blockchain solutions can enhance their brand reputation and appeal to eco-conscious consumers.

- Carbon Credit Markets: Blockchain can support transparent and efficient carbon credit markets. By recording carbon credit transactions on the blockchain, businesses can ensure the authenticity and traceability of their sustainability efforts. Customers can participate in carbon offset programs with confidence, knowing that their contributions are verifiable.

A company can use blockchain to track and record its carbon emissions and sustainability efforts. Customers can access this data to verify the company’s environmental claims and make informed purchasing decisions. This transparency fosters trust and encourages more sustainable consumer behavior.

Regulatory Developments

- Standardization and Compliance: As blockchain technology matures, regulatory frameworks are expected to become more standardized and clear. This standardization will reduce uncertainty and encourage broader adoption of blockchain solutions. Businesses will benefit from clearer guidelines, while customers will enjoy greater protection and confidence in blockchain-based services.

- Privacy-Enhancing Technologies: Developments in privacy-enhancing technologies, such as zero-knowledge proofs and confidential transactions, will allow businesses to comply with data privacy regulations while maintaining the transparency and security benefits of blockchain. Customers can trust that their personal data is protected without sacrificing the benefits of blockchain technology.

Blockchain technology presents a powerful tool for businesses aiming to enhance customer experience through increased security, transparency, and efficiency. Despite the challenges of scalability, regulatory compliance, and adoption barriers, the potential benefits of blockchain are significant. By embracing blockchain, businesses can provide secure and transparent transactions, foster trust, streamline processes, and offer innovative loyalty programs and payment solutions. Looking forward, the integration of blockchain with AI and IoT, along with advancements in decentralized finance and interoperability, will further amplify its impact on customer experience. As businesses navigate the evolving landscape of blockchain technology, staying informed and adaptable will be key to leveraging its full potential and achieving sustained competitive advantage.