ESG in aviation is not a new idea – but the stakes have never been higher. Regulatory pressure, capital markets, and corporate buyers are now demanding something the region’s airlines and airports cannot defer: sustainability that is embedded in strategy, tied to financial outcomes, and built to last. The differentiator is no longer who started first. It is who has integrated ESG most deeply into how they run their business.

There is a version of the GCC aviation story that almost tells itself. Passenger volumes are surging. Mega-airports are rising from desert ground. Gulf carriers have become defining players in global long-haul travel. By any conventional measure, the region’s aviation industry is in an era of extraordinary momentum.

But momentum, as any strategist knows, is not the same as resilience. The forces now reshaping global aviation — accelerating climate regulation, evolving investor expectations, and the mounting economics of decarbonization — do not pause for growth stories, however impressive. The question for GCC aviation leaders today is not whether sustainability will reshape their industry. It already is. The question is whether they will treat ESG as a strategic business system or continue managing it as a compliance obligation.

This distinction matters more than it might appear. ESG has been on the aviation agenda for years. Most carriers and airports across the GCC have sustainability commitments, reports, , and environmental programs of some kind. The problem is not the absence of ESG activity. It is the absence of integration. Organizations that have not connected their sustainability commitments to fleet investment decisions, capital allocation, route economics, fuel procurement, and governance structures may find themselves absorbing the cost and complexity of ESG, without capturing the potential value in financing, efficiency, resilience and competitiveness. The gap is what the next decade of competition will close – in one direction or the other.

Aviation’s Climate Reckoning Is Not a Future Event

To understand the pressure bearing down on the sector, consider the numbers. Aviation accounts for approximately 2.5% of global energy-related CO₂ emissions – a figure that understates its total climate impact when non-CO₂ effects, including contrails and nitrogen oxides, are taken into account. . Air travel demand is projected to double by 2025, adding an estimated 1.9 billion new passengers annually. Without active decarbonization, aviation emissions could triple by mid-century. IATA’s Net Zero 2050 pathway requires the sector to reduce net CO₂ emissions from approximately 900 million tons today to near zero – a transformation of historic scale.

Against this backdrop, regulators, investors, and corporate buyers have moved from observation to action. The Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) is embedding carbon costs directly into airline economics. The EU Emissions Trading System is expanding its aviation scope. SAF blending mandates – 10% by 2030, 70% by 2050 under EU ReFuelEU – are proliferating across Europe and beyond. More than 70 jurisdictions now operate some form of carbon pricing mechanism. And over 30% of corporate travel buyers actively require sustainability disclosures and decarbonization commitments from the carriers they book.

“ESG is no longer a peripheral sustainability agenda. It is a strategic priority shaping long-term competitiveness, resilience, and access to capital across the aviation industry.”

For airlines, this translates directly into financial exposure. Carbon pricing mechanisms are converting emissions into balance-sheet costs. The economics of Sustainable Aviation Fuel (SAF) — currently two to five times more expensive than conventional jet fuel — are reshaping procurement and fleet strategy. And the sheer capital intensity of the transition — IATA estimates that the aviation sector will require between USD 3 and 5 trillion in transition investment by 2050 — means that access to sustainable finance is becoming a competitive variable, not just a financing consideration.

Aircraft lifecycles of 20 to 25 years mean that capital and fleet decisions made today will lock in emissions and cost structures for a generation. The decisions that aviation executives make in the next five years will echo across the next three decades. That is the nature of this transition’s urgency.

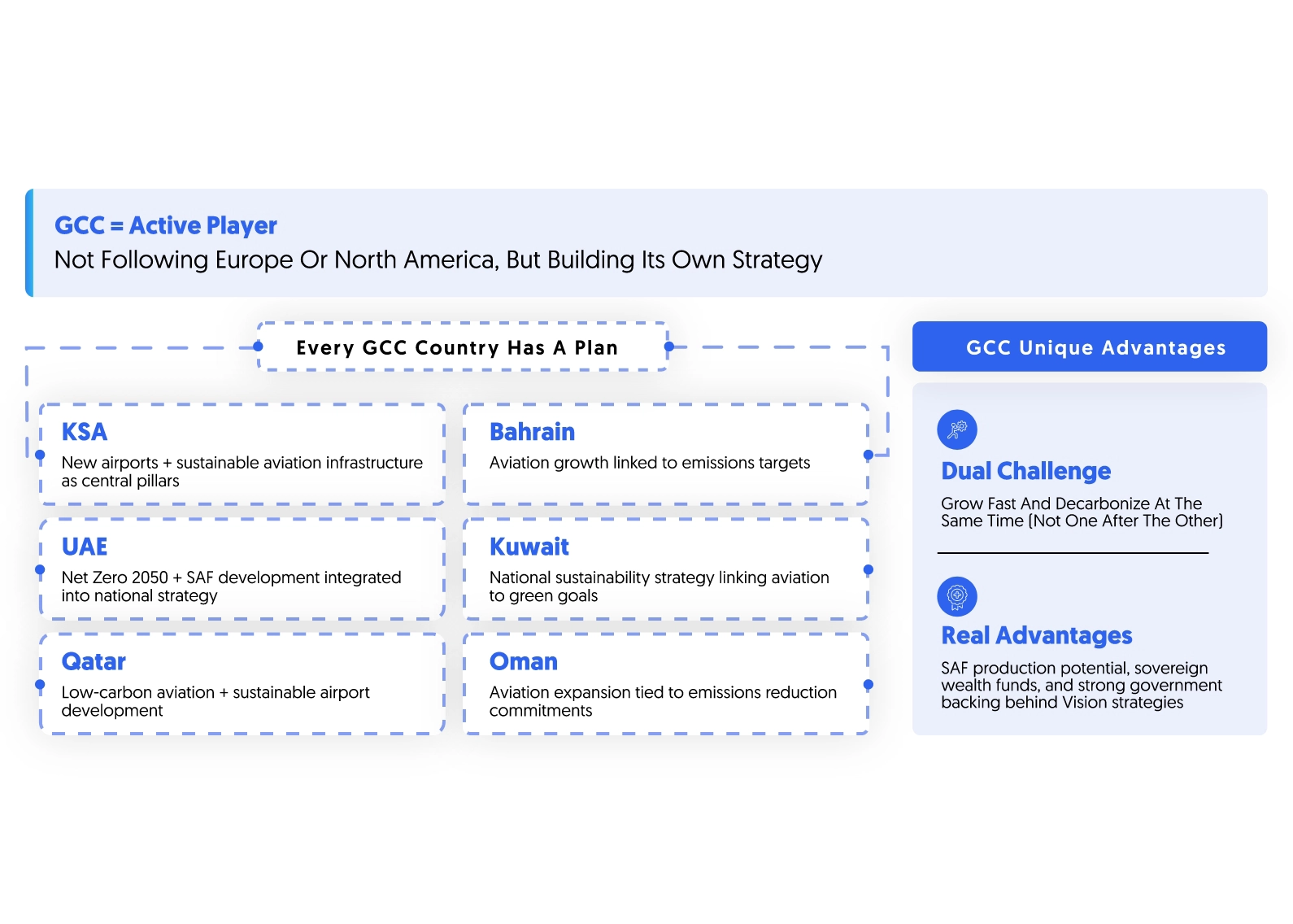

Why the GCC Is Different — and Why That Matters

The global aviation ESG story has largely been told through the lens of European regulation and North American investor pressure. But the GCC is not a passive recipient of that narrative. It is an active protagonist — with its own distinct dynamics, its own strategic assets, and its own compressed timeline for action.

The region’s aviation ambitions are extraordinary by any measure. Saudi Arabia’s Aviation Program aims to position the Kingdom as a global aviation hub, targeting 330 million passengers annually from more than 250 destinations by 2030, while expanding airport infrastructure, logistics capacity, and long-term sustainability. In the UAE, the Net Zero 2050 agenda is increasingly being translated into aviation-specific action: the General Policy for Sustainable Aviation Fuel sets a target to develop 700 million liters of local SAF production capacity annually by 2030, alongside a voluntary target for locally produced SAF to represent at least 1% of fuel used by national airlines at UAE airports by 2031. Qatar is also advacing low-carbon aviation initiatives and sustainable airport development. Across Bahrain, Kuwait, and Oman, national sustainability strategies are increasingly creating a strong link between aviation growth, resources efficiency, and emissions management.

This creates a distinctive strategic tension for the region: GCC aviation is scaling at historic speed while being asked to decarbonize. For carriers and airport operators, this is not a sequential challenge — grow now, decarbonize later. It is a concurrent one. The infrastructure being built today, the fleets being ordered, the energy partnerships being formed, the supply chains being developed must all of t be designed with the sustainability transition already

in mind.

There are, however, genuine advantages available to GCC players that are not equally available elsewhere. The region’s energy resources, renewable-energy potential, industrial capacity, and aviation demand profile position it to play a meaningful role in the future of SAF economy, particularly as pathways such as power-to-liquid fuels mature. Sovereign wealth funds and state-backed investment platforms provide access to long-term capital that can fund long-cycle transition investments. And the alignment between national Vision strategies and aviation ambition means that sustainable aviation infrastructure is not only an environmental priority; it is increasingly part of the region’s economic diversification, industrial policy, and global competitiveness agenda.

The Landscape: Who Is Moving, and How

Across the GCC aviation ecosystem, sustainability momentum is real and growing — even if integration into core strategy and financial planning remains, in many organizations, nascent.

Emirates has advanced high-profile SAF trials and operational efficiency programs, establishing itself as one of the region’s most visible aviation sustainability actors. Etihad has also built strong credibility through its modern fleet strategy, fuel-efficiency focus, and participation in SAF and low-carbon aviation initiatives. Saudia is investing in next-generation fleet modernization. Kuwait Airways has begun articulating sustainability commitments aligned with national climate objectives. Hamad International Airport is advancing energy efficiency, waste reduction, and carbon management programs. Oman Airports is developing environmental management frameworks. Bahrain Airport Company has launched sustainability initiatives targeting emissions and operational footprint.

These are meaningful steps. But they are, for the most part, still individual initiatives rather than integrated transformation programs. What distinguishes the leading global aviation organizations is not the ambition of their sustainability commitments — it is the depth of integration: net-zero targets embedded into financial planning, decarbonization roadmaps that drive fleet investment decisions, carbon cost modelling that shapes route economics, and ESG governance with board-level ownership and operational accountability.

THREE STRATEGIC IMPERATIVES FOR GCC AVIATION LEADERS

01 From Commitments to Credible Decarbonization Pathways

SAF is expected to do much of the heavy lifting in aviation’s net-zero pathway, with IATA estimating that it could contribute around 65% of the emissions reductions needed for the sector to reach net zero by 2050 — dwarfing every other lever. GCC carriers and airports must move beyond general sustainability pledges toward structured roadmaps: baseline emissions measurement, SAF sourcing strategies, fleet modernization timelines, and operational efficiency programs, and supplier partnerships designed to work in concert. The region’s potential as a SAF production hub — leveraging renewable energy potential, industrial capacity and competitive energy economics — should be treated as a strategic priority, not an afterthought.

02 Integrating Climate Transition Into Financial Planning

Carbon pricing mechanisms are no longer theoretical. CORSIA and expanding ETS frameworks are translating emissions into direct and growing financial costs. Low-carbon fuels carry a cost premium that makes fuel procurement strategy inseparable from decarbonization strategy. Airlines and airports that fail to model carbon cost exposure, scenario-test SAF economics, and integrate transition dynamics into fleet and capital allocation decisions are flying blind into a heavily regulated financial environment.

03 Building ESG Governance and Reporting Infrastructure Climate Transition Into Financial Planning

Evolving global disclosure standards — including ISSB/IFRS Sustainability Disclosure Frameworks, TCFD-aligned climate disclosures, GRI, and sector-specific aviation frameworks such as SASB airlines that are raising the bar on ESG transparency. Investors evaluating GCC aviation assets increasingly apply the same scrutiny to sustainability disclosure quality as they do to financial reporting. Organizations must build thedata infrastructure, governance structures, internal controls, and reporting capabilities required to meet these evolving expectations with credible, decision-useful information.

The Business Case for Integration

The question GCC aviation leaders need to ask is not “who moved first?” It is “who has integrated most deeply?” The differentiating variable in the next decade of aviation competition will not be who published the earliest net-zero pledge. It will be which organizations have built sustainability into the operating logic of their business – and can demonstrate it with data.

The business outcomes of genuine ESG integration are concrete. Airlines with credible decarbonization strategies and measurable emissions progress gain preferential access to green bonds, sustainability linked loans, and the growing pool of ESG-mandated institutional capital – at financing terms unavailable to less-prepared competitors. Deep SAF procurement relationships, built on structured supply agreements rather than spot purchases, will prove decisive as feedstock and production capacity remain constrained through the 2030s. Corporate travel buyers – who represent a disproportionate share of airline revenue – are increasingly awarding contracts based on auditable sustainability credentials, not aspirational targets.

“The differentiator is not who started the ESG journey first. It is who has built sustainability most deeply into strategy, financial planning, and operational decision-making.”

On the risk side of the ledger, the exposure is equally concrete. Physical climate risks — heat events affecting aircraft performance and airport operations, extreme weather disrupting route economics, flooding threatening airport infrastructure — are already shaping operational planning for airports across the Gulf. Transition risks — the combination of carbon pricing, regulatory compliance costs, and potential greenwashing scrutiny — are growing by the year. Organizations that have not embedded climate risk into their enterprise risk management frameworks are carrying unquantified, and therefore unmanaged, exposure.

This is not an argument for sustainability as virtue. It is an argument for sustainability as strategy — grounded in the recognition that the financial, commercial, and operational dimensions of the aviation transition are inseparable from the environmental ones.

What GCC Aviation Leaders Should Do Now

Urgency, to be actionable, must be translated into sequence. The following framework maps the five foundational priorities for GCC aviation organizations building credible ESG integration:

priority

01 Baseline ESG & Emissions Assessment

02 Scenario-Based Decarbonization Roadmap

03 Carbon Cost Integration into Finance

04 ESG Data & Reporting Infrastructure

05 SAF & Regulatory Ecosystem Engagement

STRATEGIC OUTCOME

01

Establishes Scope 1/2/3 inventory; enables credible decarbonization target-setting and investor-grade disclosure

02

Translates net-zero commitments into explicit transition-pathways with SAF adoption curves, fleet modernization timelines, and carbon cost modeling

03

Embeds carbon pricing into fleet, route, and capital decisions; reduces regulatory exposure

04

Enables consolidated and automated audit-ready ESG data to meet evolving disclosure requirements

05

Secures supply relationships, shapes policy dialogue, and signals capital-market credibility

Source: New Metrics ESG & Sustainability Practice

Develop a scenario-based decarbonization roadmap. Net-zero commitments that are not backed by explicit transition pathways — with SAF adoption curves, fleet modernization schedules, operational efficiency milestones, and carbon cost modelling — will not withstand investor or regulatory scrutiny.

Integrate carbon costs into financial planning. Carbon pricing is not an external variable to be managed by the sustainability team. It is a financial variable that belongs in the same models as fuel costs, fleet depreciation, and route economics.

Build ESG data and reporting capabilities. Organizations that invest now in consolidated, automated, and audit-ready ESG data systems will be better positioned to meet evolving disclosure requirements — and to use sustainability data as an active management tool.

Engage proactively with SAF ecosystems, regulators, and capital markets. Building partnerships with SAF producers, engaging constructively with regulators, and signalling credible commitment to capital markets are strategic actions that compound over time.

Sustainability as a Performance System, Not a Reporting Function

There is a version of ESG that aviation organizations have been practicing for some years: the version defined by annual sustainability reports, carbon offset purchases, and aspirational net-zero pledges attached to distant target dates. That version of ESG is not without value. But it is not what the next decade of aviation competition will reward.

What the next decade will reward is the integration of sustainability into the operating logic of aviation organizations — into fleet investment decisions, fuel procurement strategies, route economics, capital allocation frameworks, risk management processes, and governance structures. Not ESG as a function that reports to the sustainability team, but ESG as a performance system that runs through the entire business.

The GCC aviation sector has the ambition, the capital access, the government alignment, and — in some cases — the strategic assets to lead this transition rather than follow it. The region’s carriers and airports could become exemplars of what integrated sustainable aviation looks like in an emerging market context: organizations that proved it was possible to grow boldly and decarbonize credibly at the same time.

That outcome is achievable. But it requires decisions made now — with the clarity that this is not a peripheral ESG agenda, but the central strategic challenge of the decisive decade ahead.

The organizations that treat this moment as an operational inconvenience will cede ground to those that treat it as a strategic opportunity. The skies ahead are being designed today.

About the author

Sarah Safi, is an environmental economist with over 12 years of experience in ESG and sustainability consultancy, supporting public and private sectors in achieving their sustainability goals. As a Principal at New Metrics, she leads innovative ESG and sustainability services, combining digital solutions and advisory expertise to help organizations drive impactful change.

about new metrics New Metrics is a leading human-centric transformation consultancy helping organizations across the GCC turn sustainability into a business system — not a reporting function. Our ESG & Sustainability practice supports airlines, airports, and aviation ecosystem players across the full transition journey. newmetrics.com

$100B+ Committed GCC aviation infrastructure investment across the region’s national strategies to 2030

65% Estimated contribution of SAF to aviation decarbonization by 2050

70+ Jurisdictions operating carbon pricing mechanisms globally

GCC Aviation ESG Momentum

» Saudi Aviation Strategy integrates SAF development and sustainable airport infrastructure

» UAE Net Zero 2050 explicitly includes aviation decarbonization targets

» Qatar advancing low-carbon airport development and climate commitments

» Emirates leading regional SAF trials and efficiency programs

» Hamad International advancing energy efficiency and carbon management

» Oman Airports developing environmental management frameworks

New Metrics Aviation ESG Services

» ESG Strategy & Transformation

» Decarbonization Pathways & SAF Strategy

»Climate Transition & Financial Decision-Making

» ESG Risk & Integration

» ESG Reporting & Disclosure